Quantitative Short Selling is Still Free Money... Kinda.

This shouldn't work, but it does. Welcome to quant land.

At The Quant’s Playbook, we take market opportunities very seriously. If we even get a whisper that there might be alpha lurking in some overlooked corner of the market, we break our backs to verify it, and if it’s real; we push it to production as fast as possible.

Well, recently, we found something real.

Picking back up from our earlier short-selling experiment, we dove headfirst into the entire short-selling ecosystem and committed ourselves to building and deploying a strategy around it:

We started with a crude test: short the small-cap stocks showing the highest one-day volatility; no overthinking.

After verifying the historical simulation, we went straight into prod, paid some steep borrow costs, and to our surprise, did pretty well.

Eventually though, we hit a wall; one that every serious short seller runs into:

Basic retail brokers aren’t built for this.

Now, if you’re retail and looking to get into “big boy” trading, the industry standard is Interactive Brokers.

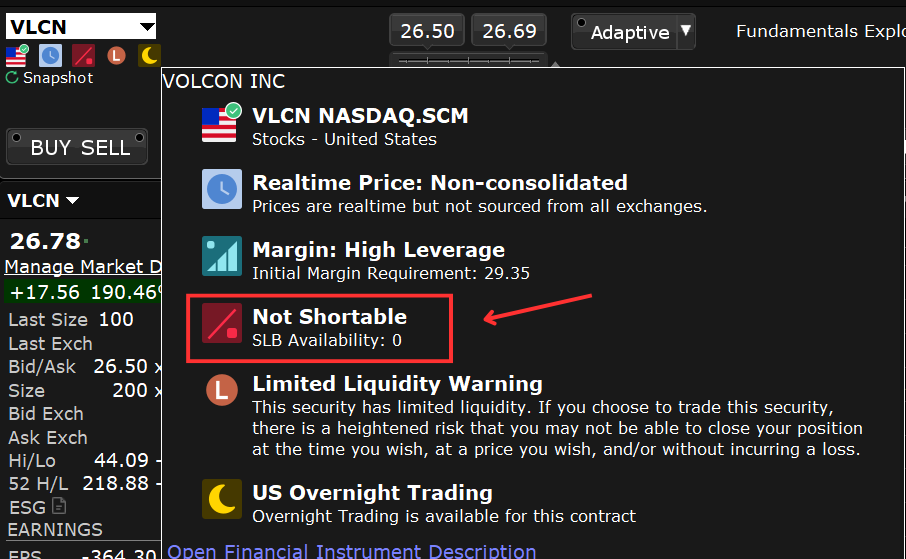

IBKR will generally let you short the shares you need, albeit at a steep borrow cost; but once you start venturing into the murky corners where the real edge lives: the $2 garbage fires, the pump and dumps — you’ll often see stuff like this:

You can sit there and watch the price drop 40% over the course of the day, but if they don’t have it, you don’t get it — period.

Naturally, being the plucky quant that you are, you think to yourself that there must be a way to be able to short the shares you need. Actually, screw the shares you need, you should be able to short anything you want.

So, after some digging, you find out that you were still a fresh-faced rookie in the short selling business and that there exists an entire network of specialized brokers that focus exclusively on short selling.

Doesn’t matter if you want to short TSLA or a $0.50 Omaha Refrigerator company — they will get you the shares.

We were already in motion when we hit this bottleneck, so the second we found out about these brokers, we signed up, deposited a sizable amount and kept trying to get our strategy back up.

Of course, as is tradition in this business, that freedom came with a price.

Today, we’re going to give you an in-depth tour of the shadow world of exclusive short-selling brokers, share a pretty interesting strategy we developed (with real trades to prove it), and dive into some damn fun quant stuff along the way.

So, without further ado, let’s get right into it.

The True Cost of Freedom

Alright, you’re a fresh-faced quant looking to dip your toes into short selling. You think to yourself:

“There’s always a handful of stocks that double in pre-market, only to fizzle out by the close. Why don’t I just short those?”

You run a quick, transaction-cost-free backtest and the results look killer. So, naturally, you jump straight in to see what the real-world costs actually are.

You fire up your production script, generate your daily basket, and head over to your broker — ready to pounce.

But before you can even risk a single dime, you’re hit with a message from your broker:

Upon returning to Earth from your rage, you put in a bit of elbow grease in search of a way to short these shares and eventually, you wind up at TradeZero (no affiliation).

You search for the same stock you were blocked from shorting and quickly realize this is a whole different game.

With specialized brokers like these, the model is flipped. You don’t just borrow shares that are available; you pay upfront to locate them:

The cost of a locate is typically charged per share, and most of these brokers require a minimum request — usually 100 shares. Just like traditional borrow fees, the cost changes based on demand and how difficult the shares are to source.

If it’s a low-float name with only 30,000 shares outstanding, expect to pay up.

Think of a locate like an option: you're paying for the right, not the obligation, to short the shares.

Say you’re offered a locate for 100 shares at a cost of $120. At that point, you’ve got three choices:

Use the locate and submit a short sell order for those shares

Credit the locate back to the system (sometimes possible)

Let it expire unused at the end of the day

Now, in the above example, the cost for getting the ability to short 100 shares was $120. We can run a quick test on what that’s costing us right off the bat:

100 shares * $25.48 = $2,548 notional exposure

$120 fee on that → 5% of total size (120 / 2.5k)

Now, as we covered in our first intro to the short selling business, this isn’t really that big of a problem. The expected variance of shorting garbage hovers around 15-20% per day, so that 5% hurdle is easily beatable.

The bigger issue is that this creates a kind of pseudo-barrier. Let’s say you’re starting with the $25,000 minimum needed for intraday trading. If you only want to risk 1% of your account on a single name, that’s $250.

But remember: you already paid $120 for the locate. If you only put $250 into the position, you'd need the stock to drop nearly 50% just to break even. To keep the breakeven around 5%, you’d need to short the full 100 shares, which puts about 10% of your total account on the line.

That kind of sizing might make sense in a high-quality momentum portfolio, but for shorting explosive small caps? That’s just reckless.

That said, the cost of this locate was an edge case and not the norm.

Just one day later, after the stock cooled off, the same locate became dramatically cheaper:

We’ve also encountered cases that add even more friction — like stocks under a short-sale restriction (SSR), which means any short order must be placed at a price above the last traded tick.

In the example below, we had a stock that was both hard-to-borrow and under an active SSR. Nevertheless, the locate was surprisingly cheap: just $1.35 for $130 worth of short exposure — roughly a 1% breakeven:

Single-use locates like this are often cheaper because once you pay, you’re obligated to short the shares; no backing out.

Locate pricing, in general, can swing wildly throughout the day as demand and supply shift, but operationally, it’s fast: it only takes about two seconds to quote and accept a locate.

So, at this point, we had conquered a major constraint: we could short anything we wanted — stocks, warrants, ETFs — whenever we wanted.

With that complete, this brought us back to the real challenge: actually being right.

Thankfully, after a lot of leg work, we were able to put together a pretty robust framework that we’ve already taken live.

Now, we’re usually pretty open about our strategies, often going as far as publicly open sourcing them entirely — but as you’ll see in a moment, there are a few details we have to keep close to the chest.

Stuff We Should Probably Keep to Ourselves

At a high level, we’re just shorting pre-market pump-and-dumps.

Sure, we could dress it up with some rationale like:

“Due to limited liquidity in early pre-market trading, price discovery tends to be inefficient and diverges from fair value — a mean-reverting dynamic we aim to exploit.”

But really, we’re just doing the “obvious” — and it works.

Keep reading with a 7-day free trial

Subscribe to The Quant's Playbook to keep reading this post and get 7 days of free access to the full post archives.