A Junior Quant's Guide to Corporate Actions

There’s serious money to be made in SEC filings; the catch is, you actually have to read them.

To quickly bring you up to speed: we have fallen in love with short selling.

Once we beat the constraints of most retail brokers and figured out how to short virtually anything we wanted, we launched a blitzkrieg to explore what strategies we could build on this newfound access.

But this time, we knew better than to take a raw data-hacking approach.

When developing trading strategies, it’s essential to begin with a plausible, baseline rationale for why a price move might occur in the first place.

So before touching a single row of data, we asked ourselves:

“What known events result in predictably lower returns?“

Eventually, we landed on one of the most reliable drivers of large price moves: corporate actions.

Corporate actions are just the umbrella term for all events a company reports:

Earnings

Share splits

Dividends

Dilution events 😏

Management changes

What makes these events especially attractive is that they occur on defined dates, which makes applying a systematic strategy intuitive; for example, “short for n days after the event on date t.”

Now, in this business, most ideas go nowhere.

So we live by a fail-fast operandi:

data collection → crude backtest → small-scale prod.

Once we formed a baseline theory around a particular corporate event, we ran a simple simulation and then jumped straight into production to see what the real-world results looked like.

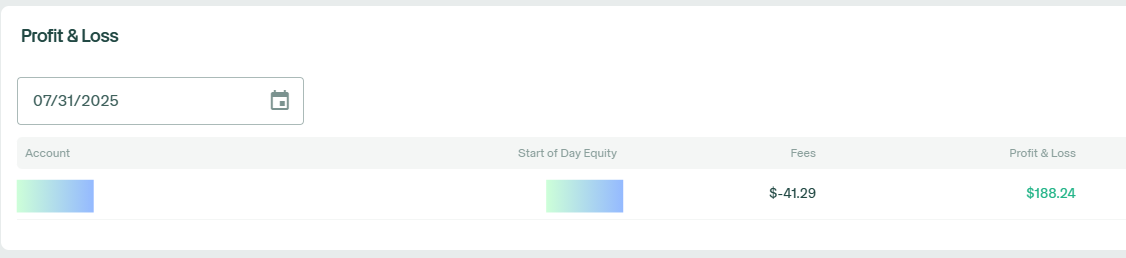

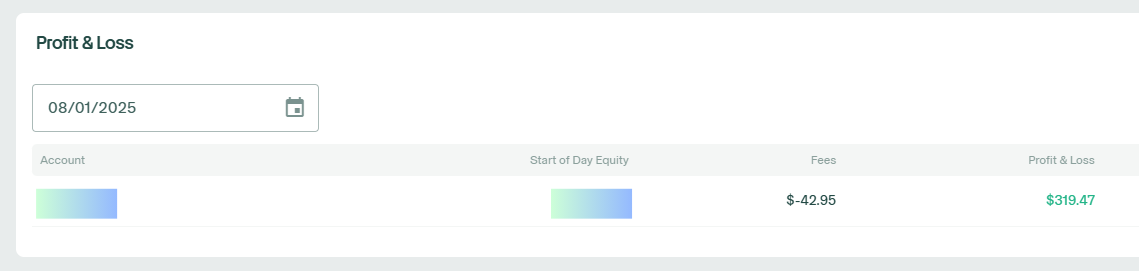

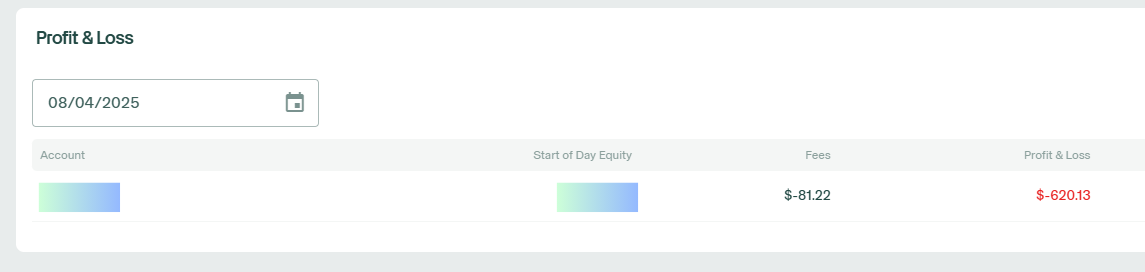

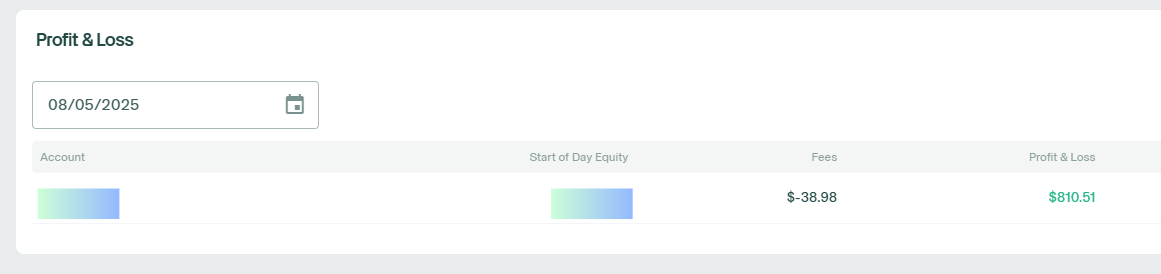

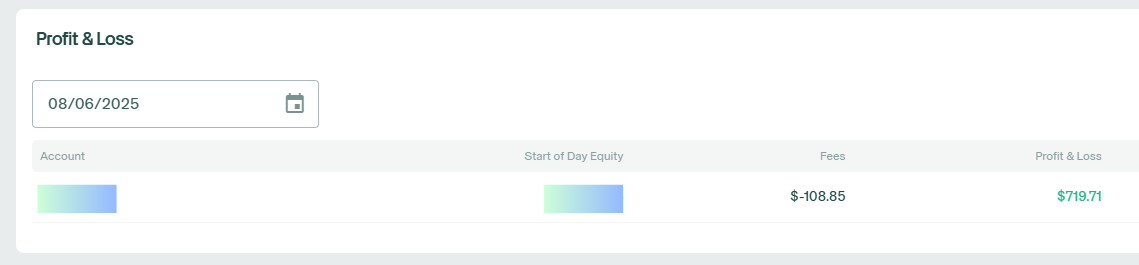

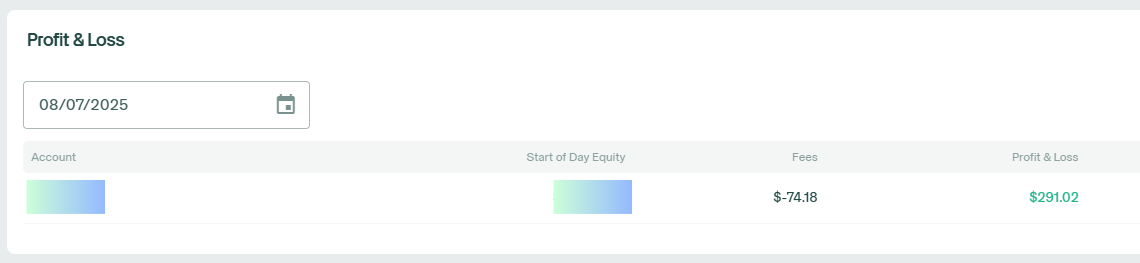

To our pleasure, this started off a sequence of extremely profitable trading, as briefed below (apologies for formatting):

Now, this corner of the market — event-driven short selling — has legitimate alpha and capacity, but there are some serious nuances that you need to know to understand why the edge exists.

So today, we’re walking you through the full, real-world process of turning these murky filings into actionable trades: from ideation and data collection, to simulation, and ultimately, live capital deployment.

As always, we’ll share the code and tools so you can replicate (or debunk) everything for yourself.

Without further ado, let’s get right into it.

You’ve Gotta Read The Filings, Man.

Before we dive into the deep end, let’s start with the basics.

Our objective is to expand our reach in the short-selling business.

We want to know when a company does something bad and place ourselves in front of the inevitable.

So, we asked ourselves:

“What kinds of events are considered “bad” by the market?”

Well, for one, take dilutive events.

Here’s how it works:

Company A starts with 10 shares, each priced at $10 → Market cap = $100.

The company issues 40 new shares → Total shares = 50.

No new value is created → Market cap still = $100.

The new theoretical share price becomes $2 ($100 ÷ 50 shares).

Existing shareholders are diluted and now own a smaller % of the company.

You’ve probably seen this play out with certain meme stocks, where a huge retail-driven run-up is quickly followed by a new share offering. The company takes advantage of the inflated price to raise capital; after all, they do generate net usable cash from these offerings.

But almost invariably: companies don’t do this from positions of strength.

Dilution is often a last resort, used by companies that:

Can’t access the bond market

Operate in high-risk sectors like biotech, where cash = runway

Are trying to prolong the inevitable bankruptcy

So, at this point, we can form our first hypothesis:

If a company dilutes their shares, the forward returns post-dilution should be negative.

Given our specialized broker access to locate and short the shares, we can plausibly execute short-sales and capture those negative future returns.

Now, that we have the idea, let’s get some data.

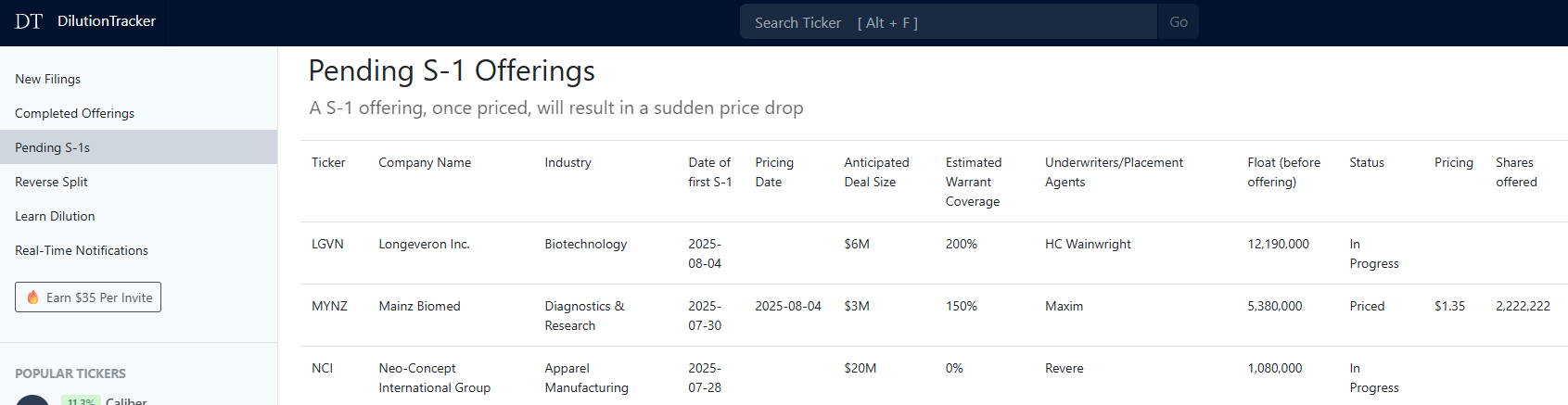

We’ll start with a dataset from DilutionTracker (no affiliation):

You see, when a company plans to dilute their shares, the price doesn’t always drop right away. It usually happens in stages, like this:

The company files a registration statement with the SEC, announcing its intent to issue new shares. This doesn’t guarantee anything, it’s just a heads-up that dilution may be coming.

S-1/A Amendment

If the offering progresses, the company submits an amended filing with updated terms regarding pricing, share count, or selling shareholders. Still, there’s no guarantee the deal goes through.

Form EFFECT

Once everything’s finalized, the SEC issues an EFFECT notice. This means the offering is now legally effective and the shares can be sold.

Once this is out, the stock price immediately drops.

Because the offering might be delayed, canceled, or have its terms amended, the market doesn’t immediately price in the dilution.

So, now that we have our target event, there are a few paths we can take to form a strategy:

(A) Build a model to predict whether the share offering will be confirmed within 30 days.

Since the price often doesn’t drop on the initial S-1 filing, we could pre-position before the EFFECT form hits, then buy back after the drop.

(B) Short the day after the initial filing and hold for 30 calendar days.

Here, we’re betting, lightly, that the offering will be priced quickly, but more importantly that the filing itself marks the company as “bad”, and thus likely to produce negative forward returns.

Having faced this juncture countless times, experience says start with option B, then if the baseline crude results are good, we can then add a refinement layer.

If the simplest version of the strategy doesn’t work, optimizing it often becomes putting lipstick on a pig.

DilutionTracker’s dataset covers all non-IPO S-1 filings for micro and small-cap stocks, so we’ll use that for our first test:

On the next trading date after a dilutive S-1 filing is made, we establish a short position at the close.

We’re not aiming for HFT speed, so we implement a realistic delay of when we’d actually be able to trade.

30 calendar days later, we buy the shares back.

Repeat.

Here’s how that basic test performed:

Keep reading with a 7-day free trial

Subscribe to The Quant's Playbook to keep reading this post and get 7 days of free access to the full post archives.