You Can Be A Volatility King Too. [Code Included]

We're in the deep end now. Like, for real.

At The Quant’s Playbook, we aren’t braggarts. We’ve created fully proprietary strategies and insights in commodities, options and even in prediction markets — but we’ve always remained humble and kept a cool head.

But this here, is some crazy sh*t.

This week, we’ll be diving deep into one of the most esoteric corners of the option market: the volatility surface. You’re going to see first-hand how and why we build out our own in-house surface, and more importantly, how we’ll use it to haul away truckloads of cash.

If you’re excited about it — good. Let’s get right into it.

The inspiration for this experiment started off from a noble goal. It’s a new year, so we wanted to explore some new data we’d never toyed with before. Initially, this was a tougher pursuit than I expected. Some providers claimed to offer satellite data, anonymized credit card transactions, and some even offered mobile phone location data, but almost all of them were behind arguably the most frustrating thing on earth:

Most of these alternative data providers are generally geared to enterprise customers that tend to lock-in to multi-year licenses, so it makes sense that their onboarding process is lengthier than with say, Polygon or yfinance — but that isn’t what we want.

Thankfully, after some perseverance, we stumbled upon Nasdaq DataLink, formerly known as Quandl; take a look at some of their datasets:

The best part is, we can just get a subscription and start pulling the data — no compliance forms, no demos, no b.s. — so we’ll start here.

Now, while those datasets are great and all; here at The Quant’s Playbook, we aren’t your typical equity people — so, thankfully, after some more digging, an option dataset caught our eye:

We’re no strangers to volatility, but we haven’t ever really went deep into the finer points like constructing and trading surfaces — so this is the perfect starting point. Let’s peek at a sample of this dataset:

Now things are getting interesting. The dataset features information such as the IV at the ATM strike for different expirations, the slope of the structure, and things like historical close-to-close volatilities. If any of those terms sound confusing to you, don’t worry — let’s take a quick refresher on everything you need to know about the volatility surface.

The Volatility Surface

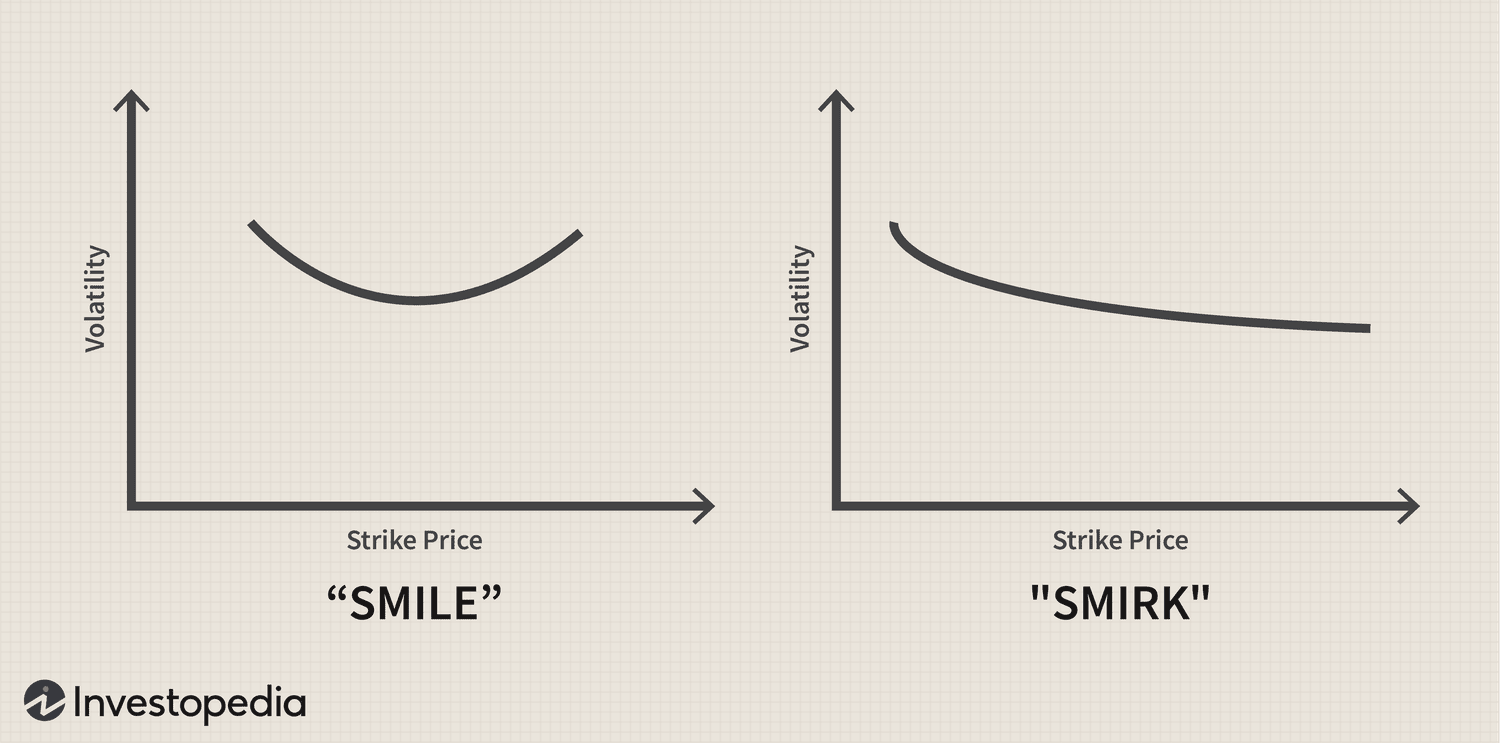

A volatility surface is simply just a way to analyze implied volatilities at different strikes and expiration dates.

Some are 3-dimensional and really cool looking:

Others are more direct and simple:

We go deeper into the specifics and industry applications here, but that’s essentially all the information you need to understand the rest of our approach.

Vol, Vol, Vol. What Do We Do With It?

It is widely agreed upon that implied volatility is a great predictor of future realized volatility:

So to us, we want to use implied volatility as a way to get a heads up on what stocks are going to move and how much they’re going to move by. Now, the most obvious way traders go with this approach is by focusing on stocks with high implied volatilities, for instance, those with upcoming earnings announcements. However, this approach is highly played out and more often than not, that anticipated boost in IV ends up being too expensive, leading to an unprofitable IV crush.

We have to be smarter.

What if, instead, there was a way to detect subtle changes and kinks in the volatility structure that would possess the same high-quality predictive power we know it for? This way, we would be able to consistently take wagers on stocks that are bound to move, but still have our positions be cheap with ample room for profit.

Well, there just might be.

Keep reading with a 7-day free trial

Subscribe to The Quant's Playbook to keep reading this post and get 7 days of free access to the full post archives.