Behind The Scenes of a Profitable Short Selling Operation

“Gravity is the cleanest trade in the book.”

For most market participants, the playbook is simple: buy quality assets, hold on, and let compounding do its work. And honestly — it’s good advice. One glance at the S&P 500 over the last decade explains why it’s become the gold standard of investing.

Now, while this works for most investors, it doesn’t fit all.

There exists a class of participant who see the market as not just a way of capital to companies, but rather a mechanism that can be systematically leveraged for personal profit.

As quantitative traders, we are that class of participant.

To bring you up to speed, we still actively run our monthly-rebalanced long momentum strategy which has continued to perform exceedingly well:

A Junior Quant's Guide to Time-Series Momentum

"You’re not predicting the future. You’re betting yesterday keeps happening."

However, when it comes to the buy-side of markets, there’s really only so much that you can do.

Our long only momentum strategy has delivered strong results, but it remains tied to the broader market. If the bull market continues, it should keep outperforming — but in a market-wide drawdown, strategies like this inevitably take a hit.

And if a trading business can be dragged into months of losses just because the market slipped, that’s not a robust business. The core mandate of quantitative trading is simple: generate profits in all conditions: up or down.

To mitigate some of that one-way risk, we began gearing our operations to focus on short-selling:

At first, we messed around with purely quantitative strategies like chasing volatility and shorting small-cap stocks that became over-extended in pre-market trading.

Over time, we shifted toward deeper structural edges: how markets react to SEC filings and corporate actions, such as dilution events revealed in S-1 filings.

That pivot made the difference.

By anchoring our strategies to clear, rational mechanisms rather than noise, we found substantially more consistent success:

We last left off describing a rather trivial implementation of short selling a stock for 30 days after a given corporate event.

Since then, we’ve taken that seed idea and scaled it into something much bigger: a daily cash engine built on short selling.

In this piece, we’ll pull back the curtain on how we do it: synthetic index construction, complex order execution, and the mechanics of turning it into real profits.

So, without further ado, let’s get right into it.

It’s Like The S&P 500, But Reversed

You’ve probably heard the idea that small traders sometimes hold an edge over large institutions. On the surface, that sounds paradoxical, but sometimes, it’s true.

To see this, let’s examine our early approach of shorting a company for 30 days after they make a dilutive S-1 filing. When a company dilutes their own shares, it’s often seen as a desperate last-option move for raising cash, so most companies don’t do it (instead, good companies tend to buy back shares, reducing total float — the opposite of dilution).

These moves happen most often in nano-caps on the brink of delisting. A $40B hedge fund might see the same signal and know that the stock is headed lower, but they can’t size into a $50M market cap without distorting it or eating massive slippage; so they pass.

Smaller traders don’t have that constraint. You can press $100K into a setup like this; a rounding error to a megafund, but a high-expected-value trade for those willing to scoop up the scraps.

Of course, though, with every pro comes a con.

Shorting $5 nano-caps looks linear most of the time — until you meet the grim reaper: tail risk.

To see an example of this, let’s take a look at Forward Industries (NASDAQ: FORD):

In the market regime at time of writing (Q3 2025), it’s become a popular trend for stale, under-the-radar companies to announce that they’re running some new “crypto treasury” strategy, sending their shares higher on the news. A few days later, an SEC filing follows, revealing that the company is raising cash at those elevated levels. Not long after, the price drifts back down and the company is never heard from again.

The big picture is clear, but the risk remains that any one of these names could rally 10x on a gimmick theme before reality sets back in.

While these blowups are the exception rather than the rule, you can’t build a viable business if one day you wake up and lose 10x your capital for no good reason.

So, that sparked an idea:

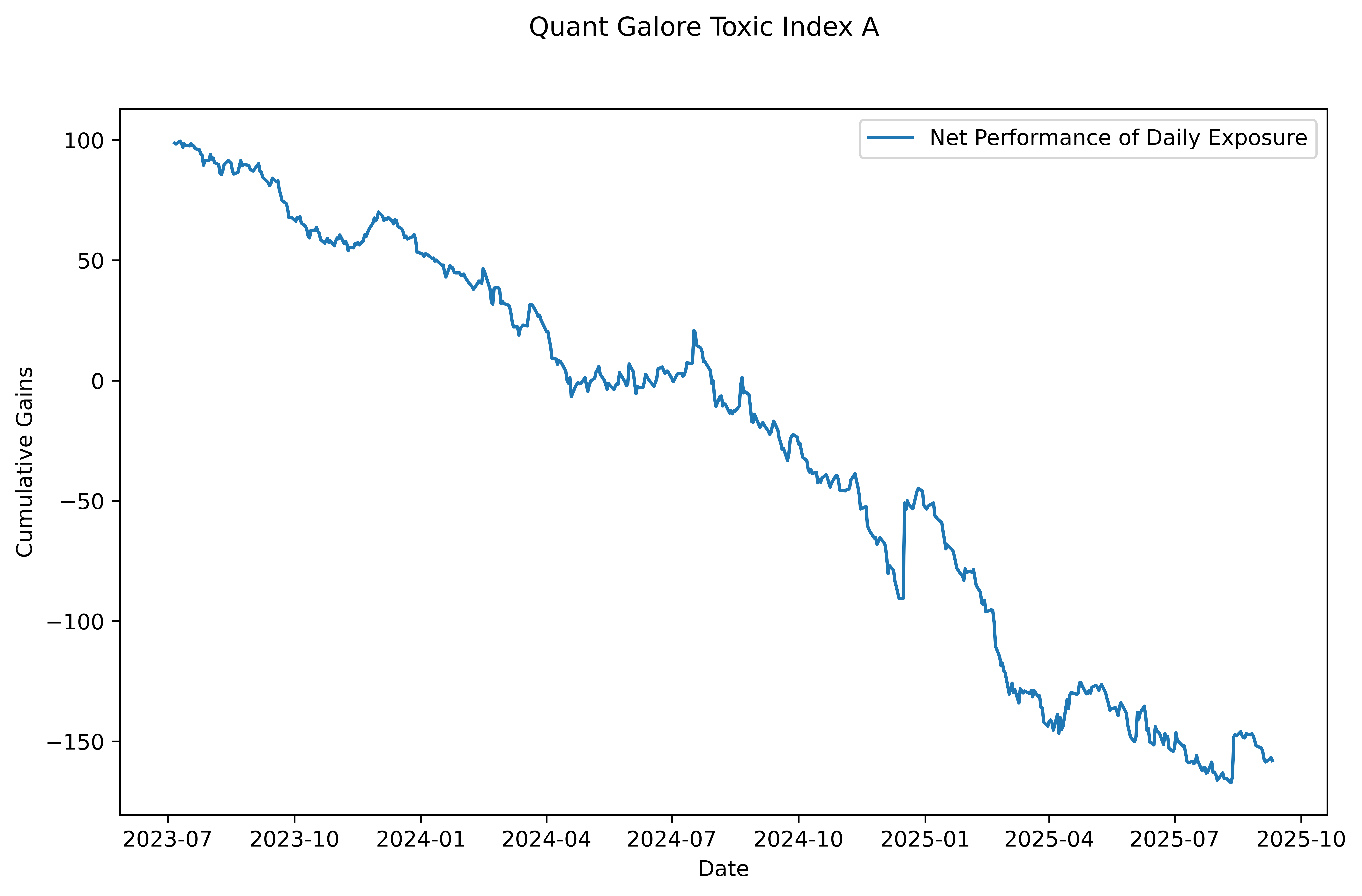

What if instead of taking these single-stock wagers, we created an index of hundreds of these “toxic” assets to continuously short?

Idiosyncratic risk is unavoidable by nature, but it is largely hedge-able through sufficient diversification. So, what if we just created an inverse S&P 500 — instead of the 500 best companies, what about a universe of liquid, toxic companies only?

Such an index would virtually be a straight line down; but as a short seller, that’s the point. If we created such an index, we would aim to replicate it daily through short sale exposure by shorting the individual components.

Now, we already know that overnight borrow costs can be steep, so instead of just doing buy and hold, we opt for daily intraday exposure.

This has a few advantages:

No overnight borrow costs.

In the land of small-cap biotechs headed for failure, overnight borrow costs can exceed 200% on an annualized basis. While you’ll still have to incur per-share locate costs (e.g., $0.003/share), it will be dramatically cheaper than funding an overnight position.

No margin interest.

With most professional brokers, you can borrow up to 4x your starting capital under Reg-T margin. If positions are flattened before the close, there’s no interest expense.

Lower tail risk.

Idiosyncratic risk doesn’t vanish, but realized intraday volatility is generally dampened by higher liquidity and tighter spreads during regular hours; unlike pre/post-market, where thin books make stocks easier to whip around

The structure is simple: each day we borrow as much as we can, short the weakest companies, close positions by the bell, and reset to do it all again tomorrow.

Of course, in this business, the theory is the easy part. It’s execution that demands the real elbow grease.

Index Replication: Easier Than You Think

At first, the idea of buying or selling hundreds of securities at once seemed daunting. Would we have to eat the bid/ask spread on every name? How could we coordinate all the orders to go out at the same time?

Surprisingly, it’s much simpler than it sounds.

The key lies in one of the most underappreciated, but genius features of modern exchanges: opening and closing auctions.

These auctions are designed to match all eligible orders at a single, consolidated price — the official open or close of the trading day. Think of them like massive, well, auctions: every order submitted before the cutoff is considered, and the exchange determines a clearing price where the most volume can be matched.

If you’re running daily backtests with OHLC data, those “open” and “close” prices aren’t just the first or last trades of the day — they’re the actual prices set in these auctions (for daily OHLC data specifically).

To participate, you have to specify it explicitly with Market-On-Open (MOO) or Market-On-Close (MOC) orders.

Example: Say we want to short 200 names in our toxic basket at open. Instead of sending 200 separate aggressive market orders and getting picked off across 200 bid/ask spreads, we just submit 200 Market-On-Open (MOO) orders the night before.

When the opening auction fires at 9:30 AM, we’re filled at the official opening price, alongside the rest of the market — no fuss, no slippage.

This mechanism is what makes basket execution clean and scalable.

Once you're plugged into the auction logic, trading at the open or close becomes far more orderly and, more importantly, far closer to your backtest than you might expect.

The only real exception is in ultra-illiquid names where auction volume is thin (e.g., stocks with average daily notional volumes of just a few thousand dollars). Those are easily avoided with basic filters.

So, now that we have a way of getting in and out of the market with minimal slippage, the next step is generating the orders themselves.

That too is easier than you’d think.

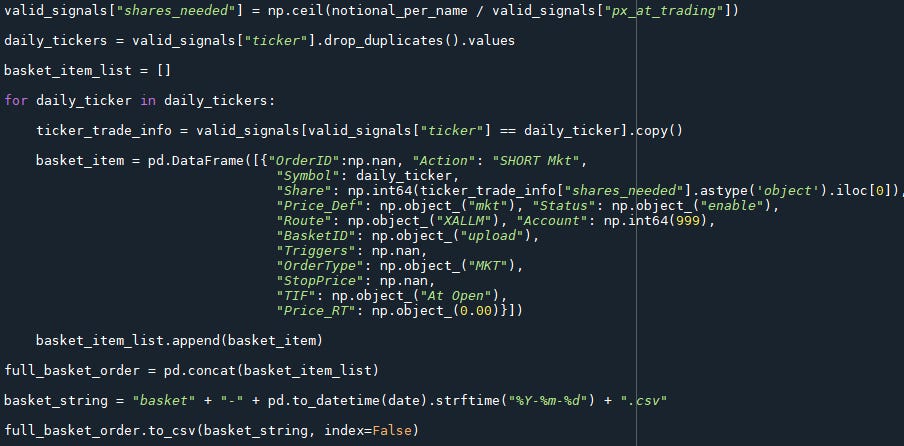

Most professional trading platforms support basket order functionality: you just upload a pre-configured CSV of orders and fire it off with a single click.

We first generate the daily basket in Python by iterating through the names in our toxic index and writing the orders for submission:

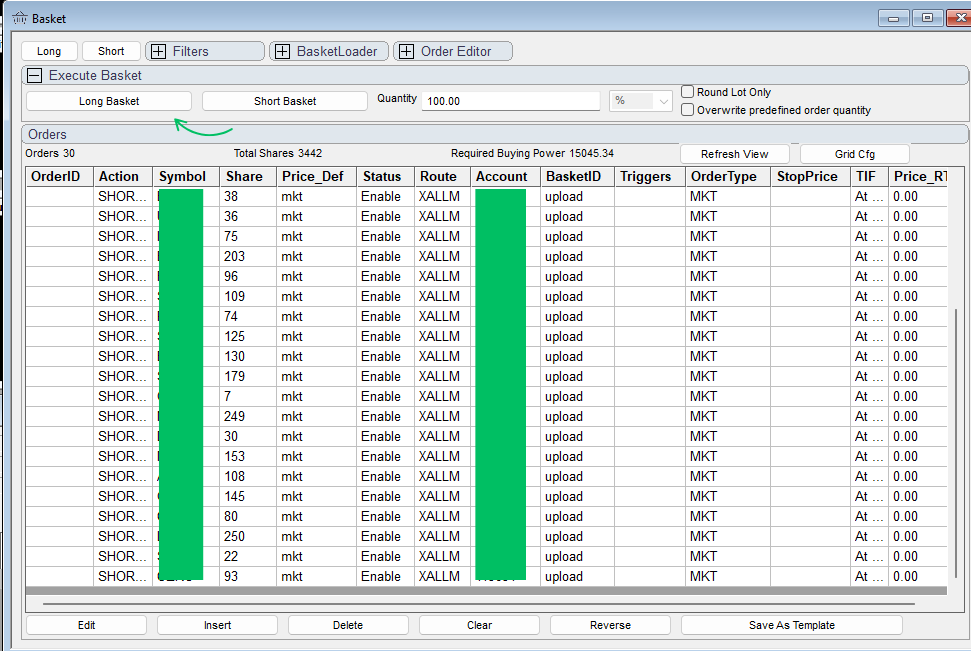

Next, we upload the file to our trading platform:

Once it’s loaded, we do a quick sanity check to make sure everything looks right, then hit execute and let the auction handle the fills.

Keep reading with a 7-day free trial

Subscribe to The Quant's Playbook to keep reading this post and get 7 days of free access to the full post archives.