The State of Volatility Address: VIX Up, Market Up

Volatility markets are doing something weird...

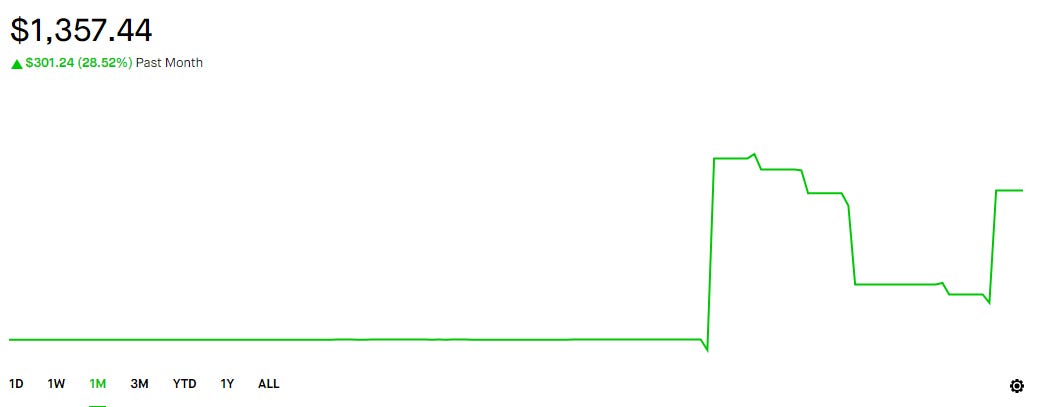

As we’ve resumed our journey back home to the wonderful land of option volatility, we’ve already stumbled on a few new quirky strategies. An update post is underway as we’re increasing our sample size — but so far we’re already up a decent bit:

However, in order to really, really enhance our profits this year, we need to take a birds-eye view of the options landscape as it currently stands.

To start, we first need to classify whether we’re in a high volatility regime or a low volatility regime. Now, if you ask 100 traders how to do this, you’ll get 100 different answers — many use a pre-defined level of the VIX, say <15 for low volatility, but we’ll go simple.

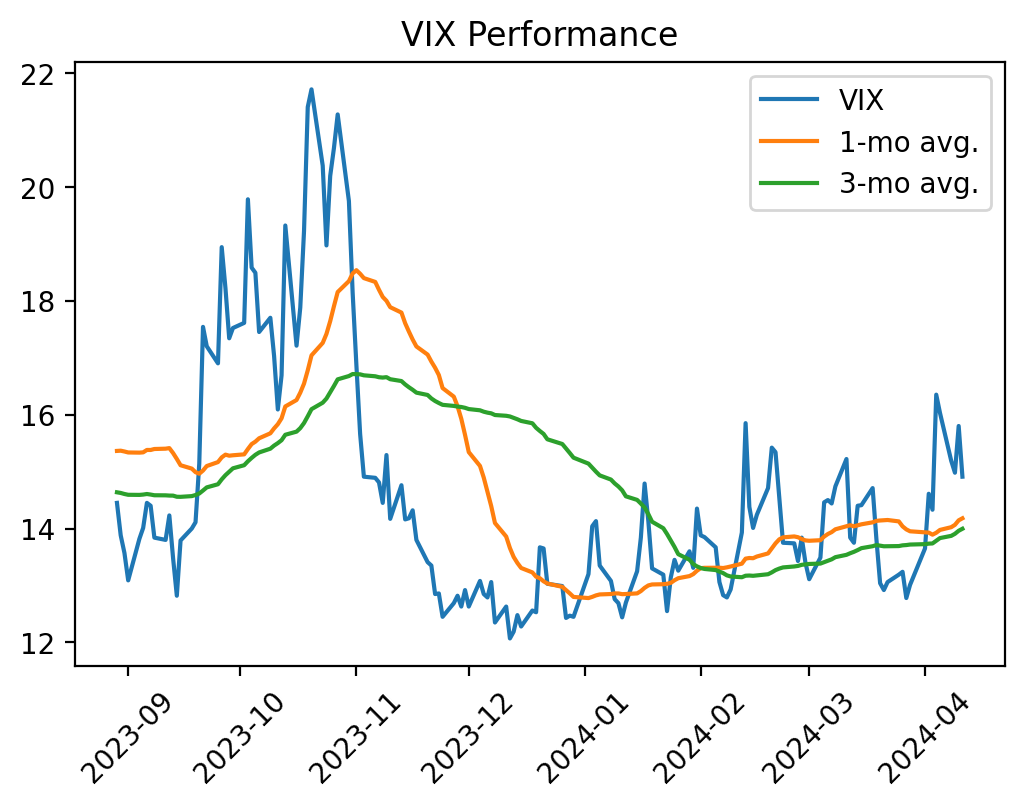

We’ve repeatedly demonstrated the efficacy of trend-following approaches, so we’ll check a simple moving average of the VIX to see how implied volatility has moved recently:

While the VIX isn’t as high as prior periods, it still seems to be in a positive trend for the year (shorter moving average > longer moving average). Remember, the VIX is a proxy for implied volatility of 30-day SPX options, so being in a positive trend essentially translates to “investors have been paying increasingly more for out-of-the-money protection/exposure”.

Despite this, the S&P 500 index is up ~8% for the year at the time of writing. This creates a relatively unusual environment of “VIX Up, Market Up”, a break from the traditional inverse relationship. So, since the current market environment has the characteristics of both high and low volatility regimes, let’s see how typical strategies of these regimes are currently performing.

To begin, we’ll start with a favorite for low-volatility regimes: selling iron condors.

We’ll design a simple 0-DTE strategy that aims to simply sell an iron condor every day — this works in low vol regimes because if the market doesn’t move greatly we consistently pocket the full premium:

At market open, we pull the open value for the VIX1D index to get the implied move for the rest of the trading day.

The VIX1D derives its value from 0-1 DTE SPX options as opposed to 27-32 days as in the original VIX. This gives us a more accurate gauge of near-term volatility.

Based on the VIX1D value, we sell an SPX Iron Condor with legs outside of that range and let it expire.

If at open, the VIX1D is, say, 15, we derive the 1-day implied move (divide by sqrt(252)) and sell an iron condor at the strikes >= ~0.94% out of the money.

We apply no fancy risk management techniques, if the options expire ITM for a loss we take it; if not, we take the full premium. On average, the maximum loss and thus collateral for this trade will be $500 (5 dollar SPX width).

Repeat daily.

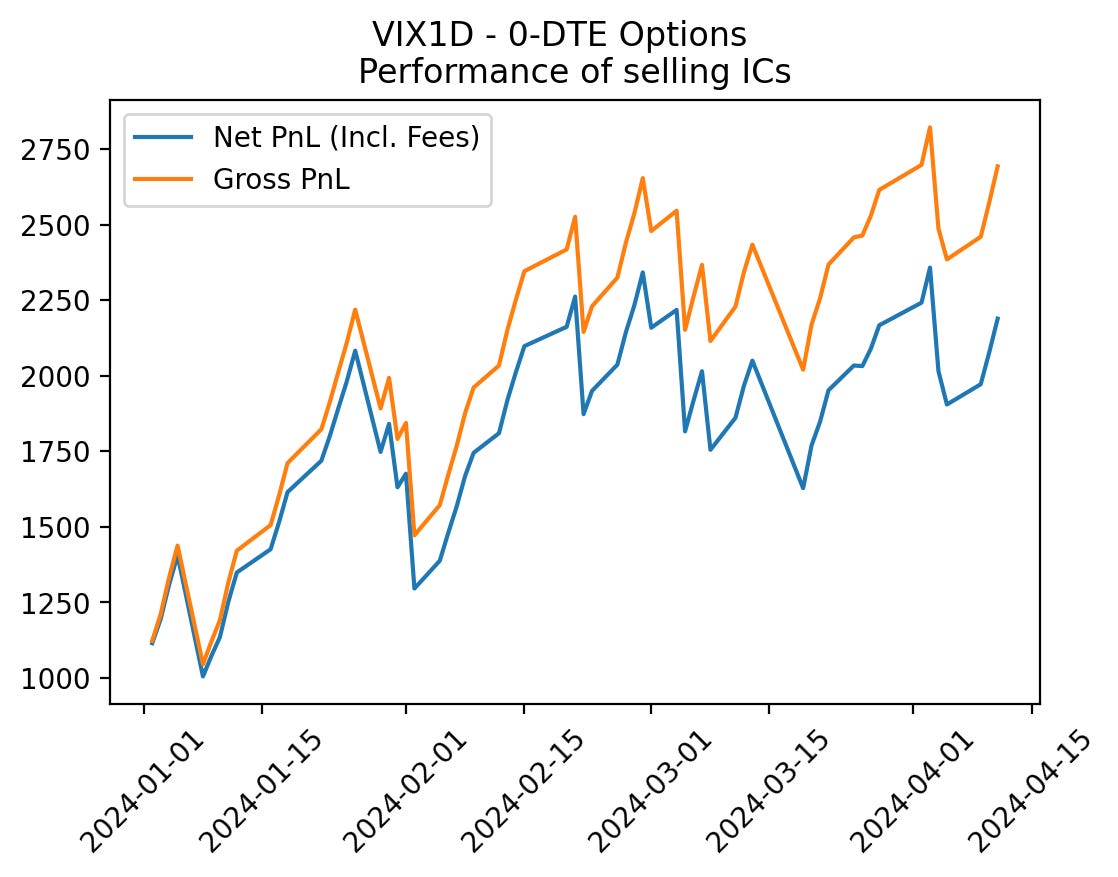

Let’s see how that’s went so far:

From January 2024 to April 11th 2024, this approach won at an ~81% rate, for an average profit of ~$100 and an average loss of ~$300.

So, even after including fees, you’d still potentially pocket about $100 a day in this current regime (80% of the time)— interesting (we may have to begin working on a short vol operation of our own).

But remember, we’re in a “VIX Up, Market Up” regime, so let’s take a look at how pro-volatility strategies perform in this same timeframe.

To do this, we’ll go with a high-volatility favorite: straddles.

We’ll keep this strategy simple:

Every day at market close, we buy an ATM straddle on SPY that expires the next day.

At market open, we sell that straddle.

Repeat daily.

Let’s see how that’s done:

From January 2024 to April 11th, 2024, this approach won at a 41% rate, with an average profit of ~$90 and an average loss of ~$46.

Here’s what happened if we traded both strategies at the same time:

Now, from a historical perspective none of this makes any sense.

When vol is low, selling premiums works at a high rate; when it’s high, buying premiums work at a high rate — but never do they work at the same time. Implied volatility is somehow both over and under stating realized volatility (Over; large iron condor premiums expiring OTM, Under; straddles generating a profit).

However, on further thought, it actually does make quite a bit of sense. To better understand this, let’s look into some more data:

Pictured above is a plot comparing what the market implied 1-day volatility to be and what volatility actually was the next day. You may not be able to tell visually, but from January to April 2024, the market over-priced next day volatility ~70% of the time! On average it over-priced volatility by ~0.40% — so, if the market (VIX1D) implied that the S&P 500 would move by 1% tomorrow, the real number would likely to be closer to ~0.60%.

This over-estimation of realized vol has a name you’ve likely heard before — the volatility risk premium. Referencing AQR’s Understanding the Volatility Risk Premium , implied volatility historically tends to be higher than realized volatility, largely due to the behavioral bias of investors being risk-averse and thus being will to overpay for downside protection (put options).

This makes sense — markets rally → investors pay extra for protection to lock-in gains → higher option prices translate to higher implied volatility → higher VIX → market continues to rally due to no fundamental economic change → VIX up, Market up.

Now, just to set the record straight, implied vol (VIX1D) might over-estimate vol often, but it’s still generally pretty accurate:

Nevertheless, our takeaway is that selling volatility in this regime works since premiums are rich, and at the same time, buying volatility works because realized volatility is high enough to make straddles profitable — a highly unusual, but magic sweet spot.

Final Thoughts

The big picture objective of this post was to shed some light into the lens we’re viewing markets through — we’ve seen that money can be made from the typical income-generating angle but we’re also seeing strong returns from both typical long-volatility strategies as well as newer, more exotic machine learning strats. We show the economic rationale behind the regime characteristics to confirm that they work for a reason, but now the job is to put it all together in the most efficient and practical way possible.

Behind the scenes at The Quant’s Playbook, we've reached a milestone where we have sufficient liquidity to meaningfully deploy multi-strategy approaches out in the real-world. This post is shorter than usual because we've been tirelessly testing various iterations of our strategies to align with our objective of daily yields and multiplicative returns, while doing our best to accurately model fees and slippage.

In the coming weeks our typical full in-depth posts will resume as we accumulate the insights from several weeks of development, we just kindly ask for and appreciate your patience as we grind it out in the home stretch.

Happy trading! 😄

So the interesting detail/nuance on how implied is both understating and overstating realized... It appears to overstate realized volatility during trading hours but understate realized overnight volatility. Almost like two different strategies compressed down to a single day. Congrats on reaching the milestone - looking forward to all the insights.