The State of Volatility Address: VIX Up, Market Up

Volatility markets are doing something weird...

As we’ve resumed our journey back home to the wonderful land of option volatility, we’ve already stumbled on a few new quirky strategies. An update post is underway as we’re increasing our sample size — but so far we’re already up a decent bit:

However, in order to really, really enhance our profits this year, we need to take a birds-eye view of the options landscape as it currently stands.

To start, we first need to classify whether we’re in a high volatility regime or a low volatility regime. Now, if you ask 100 traders how to do this, you’ll get 100 different answers — many use a pre-defined level of the VIX, say <15 for low volatility, but we’ll go simple.

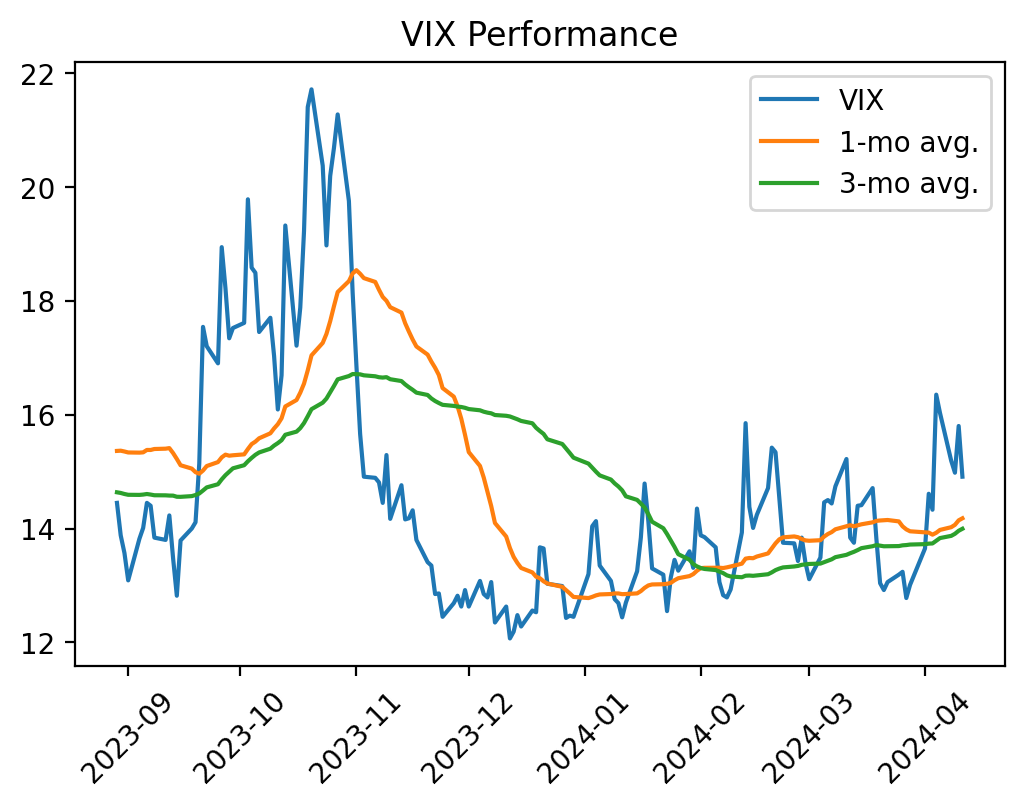

We’ve repeatedly demonstrated the efficacy of trend-following approaches, so we’ll check a simple moving average of the VIX to see how implied volatility has moved recently:

While the VIX isn’t as high as prior periods, it still seems to be in a positive trend for the year (shorter moving average > longer moving average). Remember, the VIX is a proxy for implied volatility of 30-day SPX options, so being in a positive trend essentially translates to “investors have been paying increasingly more for out-of-the-money protection/exposure”.

Despite this, the S&P 500 index is up ~8% for the year at the time of writing. This creates a relatively unusual environment of “VIX Up, Market Up”, a break from the traditional inverse relationship. So, since the current market environment has the characteristics of both high and low volatility regimes, let’s see how typical strategies of these regimes are currently performing.

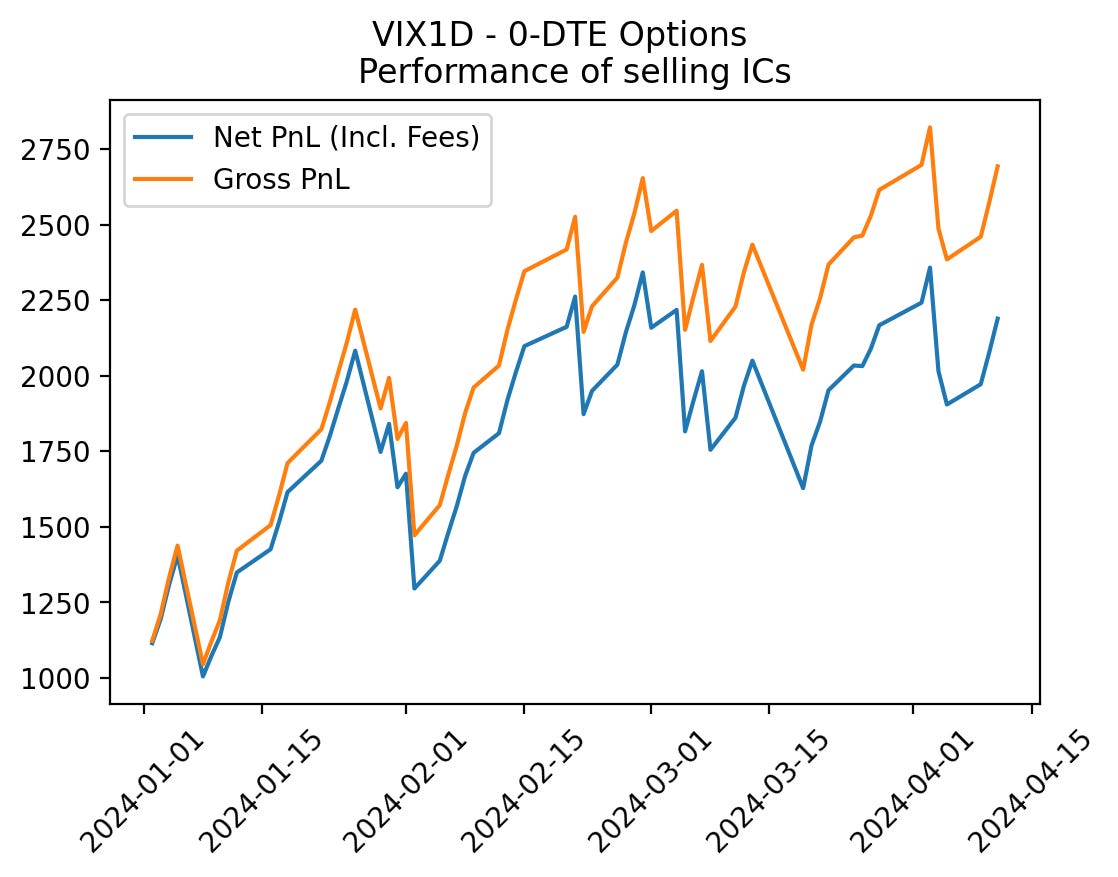

To begin, we’ll start with a favorite for low-volatility regimes: selling iron condors.

We’ll design a simple 0-DTE strategy that aims to simply sell an iron condor every day — this works in low vol regimes because if the market doesn’t move greatly we consistently pocket the full premium:

At market open, we pull the open value for the VIX1D index to get the implied move for the rest of the trading day.

The VIX1D derives its value from 0-1 DTE SPX options as opposed to 27-32 days as in the original VIX. This gives us a more accurate gauge of near-term volatility.

Based on the VIX1D value, we sell an SPX Iron Condor with legs outside of that range and let it expire.

If at open, the VIX1D is, say, 15, we derive the 1-day implied move (divide by sqrt(252)) and sell an iron condor at the strikes >= ~0.94% out of the money.

We apply no fancy risk management techniques, if the options expire ITM for a loss we take it; if not, we take the full premium. On average, the maximum loss and thus collateral for this trade will be $500 (5 dollar SPX width).

Repeat daily.

Let’s see how that’s went so far:

From January 2024 to April 11th 2024, this approach won at an ~81% rate, for an average profit of ~$100 and an average loss of ~$300.

So, even after including fees, you’d still potentially pocket about $100 a day in this current regime (80% of the time)— interesting (we may have to begin working on a short vol operation of our own).

But remember, we’re in a “VIX Up, Market Up” regime, so let’s take a look at how pro-volatility strategies perform in this same timeframe.

To do this, we’ll go with a high-volatility favorite: straddles.

We’ll keep this strategy simple:

Every day at market close, we buy an ATM straddle on SPY that expires the next day.

At market open, we sell that straddle.

Repeat daily.

Let’s see how that’s done:

From January 2024 to April 11th, 2024, this approach won at a 41% rate, with an average profit of ~$90 and an average loss of ~$46.

Here’s what happened if we traded both strategies at the same time:

Now, from a historical perspective none of this makes any sense.

When vol is low, selling premiums works at a high rate; when it’s high, buying premiums work at a high rate — but never do they work at the same time. Implied volatility is somehow both over and under stating realized volatility (Over; large iron condor premiums expiring OTM, Under; straddles generating a profit).

However, on further thought, it actually does make quite a bit of sense. To better understand this, let’s look into some more data:

Keep reading with a 7-day free trial

Subscribe to The Quant's Playbook to keep reading this post and get 7 days of free access to the full post archives.