So, I Heard Something on Flirting With Models.

Step into the fascinating world of FX Volatility.

For those that may be unfamiliar, Flirting with Models is a podcast hosted by Corey Hoffstein that aims to shine a spotlight on stars within the quantitative investment space. Episode discussions have involved high-frequency trading, scientific fixed income, and global quantitative equity strategies.

But recently, a particular episode caught my attention and introduced me to the complex, but fascinating world of FX Volatility Trading:

Before we can understand the nuances of FX Volatility, we first have to understand what makes FX options so different in the first place. But brace yourself, these aren’t your garden variety contracts.

Delta is King

From a big picture perspective, FX volatility has a lot in common with standard equity volatility:

An implied volatility value of 6% for a 1-Month to Expiration contract still implies an annualized 6% positive or negative movement in the underlying. And there is still generally a volatility smile, where contracts further out-of-the-money tend to have higher implied volatilities.

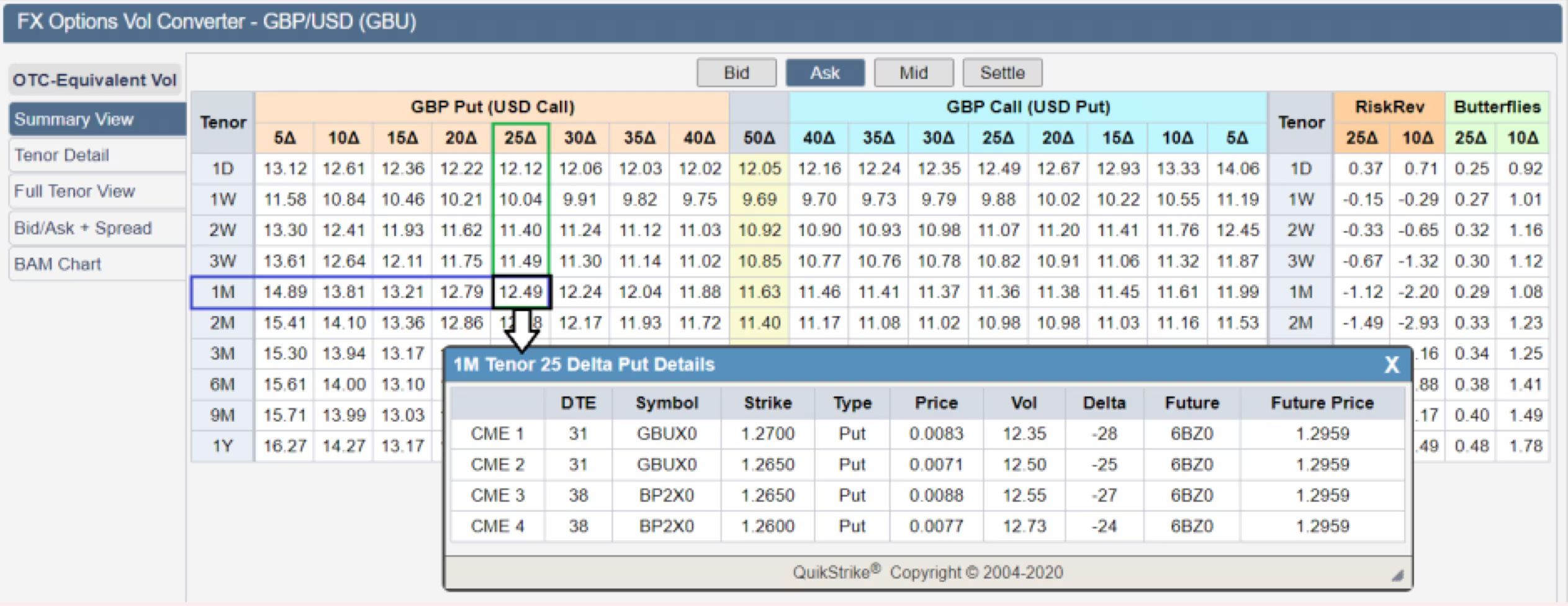

But let’s take a look at an option chain to really see the difference:

As demonstrated, instead of the traditional fixed-strikes, OTC FX option strikes are commonly quoted in terms of delta. This might appear strange at first, but let’s put our self in the shoes of an FX volatility trader to see why this convention is so advantageous:

The Mandate: Be Volatility Neutral

In this scenario, it is the big day of an economic release and in one account, you are managing an option portfolio of the EUR/USD currency pair:

As an institutional FX trader, you take these positions on not necessarily to generate a profit, but instead to make sure that you keep cash flows efficient. However, there are numerous reasons why an FX trader would need options in the first place:

Structured Products: These products are customized investment vehicles that combine multiple financial instruments, including options, to meet specific risk-return objectives. Structured products with embedded FX options can offer tailored risk exposure and potential yield optimization.

Hedging Global Exposure: For example, if Corporation A has anticipated a need for future cash flows in say, the Turkish Lira, you would buy FX options associated with that future need to protect against adverse exchange rate movements. By doing so, you mitigate the risk of currency fluctuations impacting their profits.

Yield Enhancement: In some cases, institutional traders may employ FX options as part of yield enhancement strategies. For instance, a common strategy is selling covered options on currencies they hold to generate additional income through the premium received from selling those options.

Whatever the reason for the exposure in specific contracts, one thing is clear, volatility must be avoided.

A large shock in volatility may very well be in your favor and result in a big profit, but it will be infinitely times worse if the volatility results in a significantly lower value of the book (account). If Client A needs their $10,000,000 of Swiss Francs to make a bond payment, but after the volatility shock the account notional value is $9,500,000, things become problematic quickly. Because of such high-stakes, we need to hedge out this risk to ensure that liquidity and cash flows remain stable.

Keep reading with a 7-day free trial

Subscribe to The Quant's Playbook to keep reading this post and get 7 days of free access to the full post archives.