Selling Volatility The RIGHT Way. [Code Included]

Our new short vol operation is proving to be EXACTLY what we needed.

Last week, as we were trudging along in our journey of taking our strategies into the real-world, we stumbled on something interesting. To quickly recap; as of writing, the market is in a rare regime where both short and long volatility strategies are performing strongly — vol is both rich and cheap.

Now, at The Quant’s Playbook, we’ve historically held the view that selling volatility is a no-go:

“Pennies in front of a steamroller”

“Capital intensive margin requirements”

and so on.

However, after playing with a few tests of simple strategies, we began to wonder: “Could we have been massively under-estimating the entire short vol trade?”.

Spoiler alert, we were.

In fact, what we found on a deeper look was so convincing that we immediately went live with it and have yet to be disappointed:

We’ve got a lot of ground to cover, so without wasting any more time, let’s get right into it.

*Pricing update*: As part of our commitment to being one of the few real-world, practical sources on quantitative finance, we are continuously enhancing the sophistication of our analyses/strategies and the quality of the data we use. These enhancements come with increased data, management, and operational costs. Consequently, we find it necessary to modestly increase our subscription price by $5. This adjustment will allow us to maintain the high standard of service and insights you've come to expect from us. We deeply appreciate your understanding and continued support as we make these advancements to serve you better.

God Bless The VIX

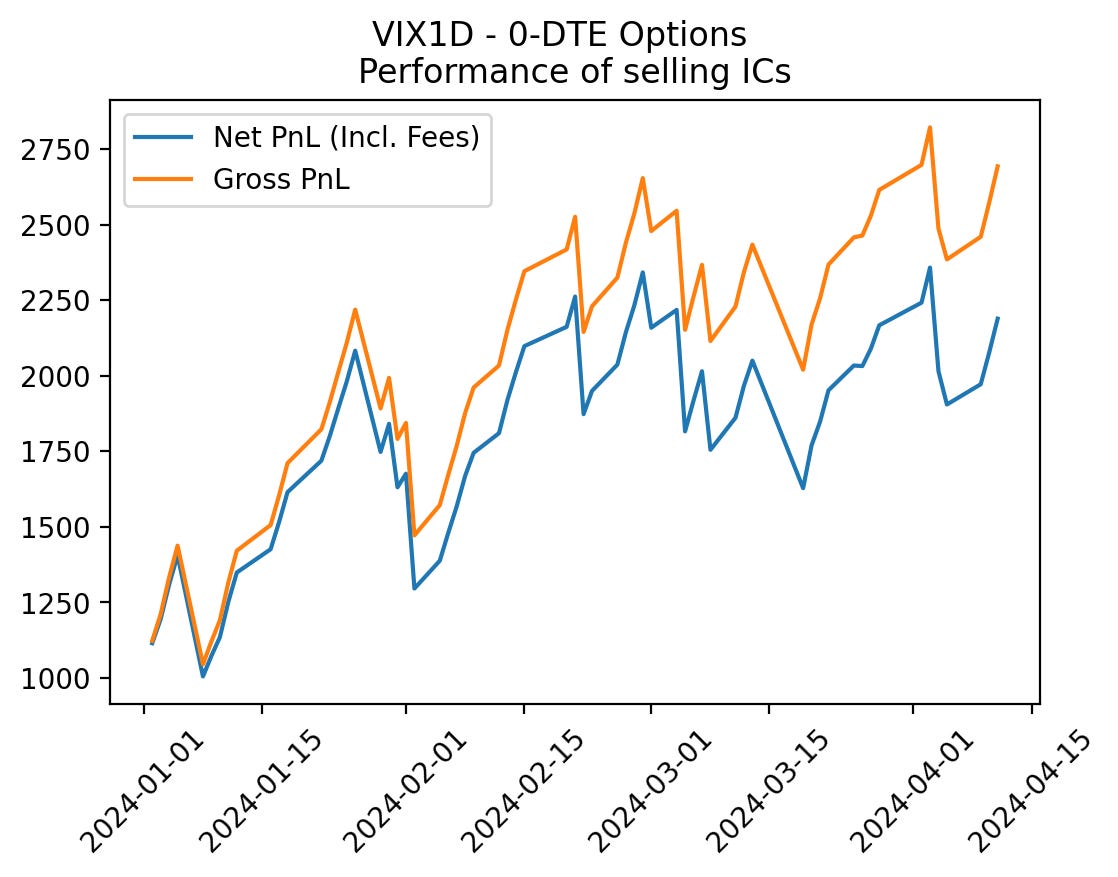

The initial jumping off point for this idea was from last week’s strategy of using the VIX1D to generate the optimal strikes to sell short. By just running an iron condor from market open to close, we generated a profit ~81% of the time:

We found that given the defined-risk nature of selling spreads, when we would take the inevitable max loss (spread width - premium), it was often equivalent to ~3-4 profitable trades. However, while unfavorable at first glance, this ratio actually gives way to a rather insane edge:

Expected Value (EV) = (avg_win * win_rate) + (avg_loss * loss_rate)

EV = (140 * .81) + (-360*.19) = $45 per trade

Now, this was already interesting, but we’ve built up quite a few tools that should help us add a bit of sophistication and take this further. So, let’s get into some of the major upgrades:

The Trend-Following Angle

We’ve been using trend-following to accurately identify positive or negative regimes and have found it to be an indispensable tool.

In theory, if we were to accurately identify that the market is in a, say, negative regime (prices falling), we would then be able to work in a directional angle as opposed to just blindly selling options on both sides.

Going with a one-sided spread (e.g., price = 100, sell 105 call and buy 110 call) would also allow us to reduce fees due to a smaller number of legs, additionally, we would keep the same high win rate since although it does have a directional bias, it’s main exposure is still short volatility (i.e., price won’t go up more than X%).

More importantly, by applying a trend following element, we make sure to not be selling puts during selloffs and selling calls during rallies.

The drawback of this approach is that instead of collecting a larger premium from selling both sides, we collect essentially 1/2 the premium by going with just one side. However, remember what we discussed about the volatility risk premium:

Keep reading with a 7-day free trial

Subscribe to The Quant's Playbook to keep reading this post and get 7 days of free access to the full post archives.