Quantitative Trading Is Awesome.

Notes From the Early Days of a Real Quant Operation

Imagine a business model where, before earning your first dollar, you must spend years building a research lab: data infrastructure, strategy development, and soft-launch pipelines just to get real-world feedback on your ideas.

A rational person might look at that structure and walk away to do literally anything else.

But not us.

As we’ve transitioned from pure research into actual live trading, our public content output has tapered, but our internal knowledge and experiential nuance have grown exponentially.

Today, we want to open the curtain and share insights that only come from being fully immersed in the trenches; insights that we guarantee you simply won’t find anywhere else.

We want to again thank you for reading, for sticking with us, and for being part of this journey.

So, without further ado, let’s get right into it.

The 35 Million Request Problem

We need to admit to something… not great.

During our research-lab phase, we wanted readers to be able to replicate our experiments in real time. This served two purposes:

To give other budding quants real, hands-on tools to work with.

To help surface any errors or blind spots in our processes.

To replicate our strategies, you needed data – specific, granular, and lots of it. We assumed we were small enough that leaving an API key or two inside a code snippet would simply give a few people a head start before they eventually built their own pipelines.

In hindsight, we had no idea how the internet actually works.

On a perfectly normal, sunny day, we received a rather serious note from our data provider:

What we intended as a quiet “leg up” for a handful of readers somehow escalated into 35 million API requests across 700+ unique IP addresses — in 30 days.

To be fair, most of this was likely from forgotten cron jobs or plug-and-play servers. But the scale was… interesting.

Rightfully, our provider immediately shut off our keys pending further review.

However, it wasn’t long before this “oopsie” turned into a genuine moment of panic.

You see, for quite some time now, our main bread and butter has been short selling.

Specifically: shorting baskets of structurally weak microcaps; the <$50M names experiencing sharp, idiosyncratic volatility spikes. It’s a niche, but a highly effective one… as long as the data keeps flowing.

So, when the access first cut off, our initial reaction was, “Okay, one day off; tough, but survivable.”

But then, the second-order effects hit us.

Our entire short-selling operation is a tightly coordinated orchestra:

Market-cap classification jobs (requiring up-to-date shares-outstanding)

SEC-filing retrieval jobs that depend on those classifications

Realized volatility forecasting jobs that depend on those filings

And finally, the daily basket constructor that depends on the forecasts

If the data stops, the whole machine stops. Not just the trades — everything. And this is just for one strategy.

A single point of failure at the provider level could take our entire infrastructure offline. For a strategy that lives and dies on early-morning responsiveness, it was simply unacceptable.

So, we bit the bullet and spun up a new subscription, temporarily increasing our operating costs by a few thousand per year. Expensive? Yes. But the alternative was worse; way, way worse.

In theory, the solution is simply “just use multiple providers.”

But in reality, market data is still fragmented, with differences in universes, schema quirks, and cost structures that make multi-provider redundancy far from trivial. With that being the case, it’s not totally unreasonable to build around one primary source.

Nevertheless, it was a rather interesting and illuminating experience.

Now, onto other matters of business.

Our Equity Trading Engine

Our core U.S. equity short-selling strategy remains largely unchanged. You can get a deeper dive of what we’re doing here:

Now, one drawback of this strategy is that the opportunity set can be relatively constrained. Some days will simply not have any prediction outputs and we thus sit it out. Some days, there are valid outputs, but there are no shares available to locate (we’re already using specialized locate brokers, so these are the super-capacity constrained nano-caps).

Most days though, we’re able to efficiently get down size and operate in a systematic manner.

However, while the opportunity set is variable, the cost of operations is not; and it only goes one direction: up.

On the surface it may appear as plain greed, but we came to think that we needed a way of continuously having at least some exposure — always, 24 hours a day, we need to be exposed to some sort of opportunity set that can keep the cashflow pumping.

With that mission set, it didn’t take long before we revisited an old friend.

Building a Crypto Desk

The beauty of crypto is that it trades 24/7, has an extremely wide opportunity set, and now with the invention of decentralized exchanges and perpetual futures, comes with the ability to run sophisticated strategies at scale.

However, the inherently decentralized nature of crypto makes building any suitable infrastructure rather challenging.

You see, with stocks, price data comes from Standard Information Processors (SIPs), corporate actions data comes from the SEC EDGAR database, and the exchanges operate within a specific time window.

In crypto, almost none of this is true:

Most idiosyncratic flow of a token is driven by Twitter accounts or other influencers.

Only the tokens with the deepest liquidity “graduate” to being listed on major exchanges

This creates a selection bias for a short-oriented trader as your universe is constrained to the “best” that were able to garner enough liquidity / interest.

There are no true “official” data sources (excluding oracles).

One data aggregator (e.g. coingecko) might combine price data for a token taken from 5 exchanges, but one of the exchanges might only include data when a trade on that specific exchange is made, so when the aggregator includes data over that period, it can end up looking very different from the prices actually observed at the respective timestamp.

In other words: the data is messy, uneven, and inconsistent.

Nevertheless, we never shy away from a challenge; after all, there is always an edge in doing hard things others aren’t willing to.

So, we’ll walk you through how we were able to establish a small foothold in the space.

Porting Equity Models Into Crypto

At the end of the day, crypto is a market like any other: certain assets behave in certain ways for specific reasons.

So, we figured that to start, we’ll just port over some equity trading logic.

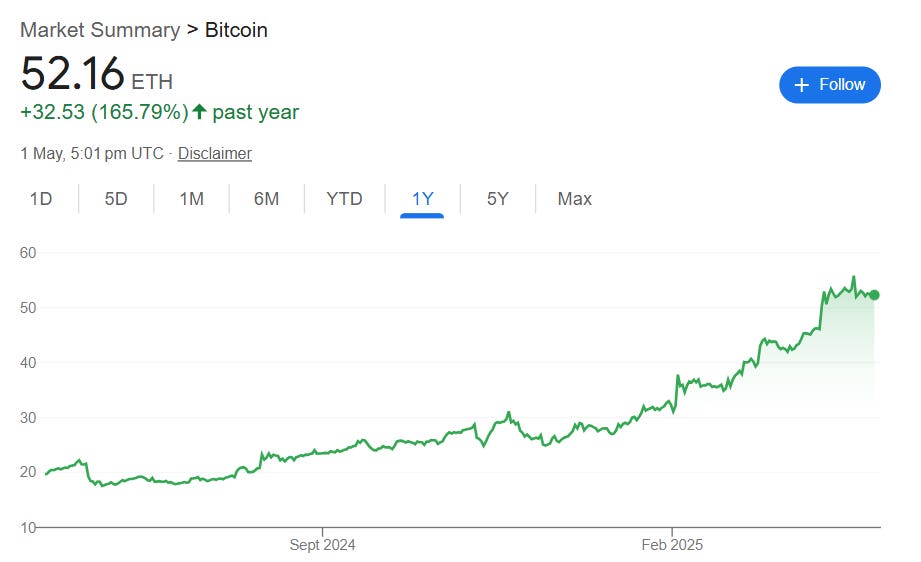

On our first venture into the space, we explored a simple strategy of simply going Long BTC and short ETH. The rationale was that this was effectively a relative value trade between the S&P 500 (BTC) and the Russell 2000 (ETH).

Now, for awhile, this was an extremely effective and high-sharpe trade:

Eventually though, the trade experienced a massive unwind and has since struggled to recover:

Although, this sucked, it didn’t really change anything about the core mechanism of a long-short strategy.

So, we thought:

“If Bitcoin is the bellwether of crypto, perhaps we just needed to be more creative in what we shorted against it.“

The rationale for choosing ETH was that it was the “little brother” of Bitcoin, but with some effort, we could probably find something with a stronger reason for why the trade should exist.

After some experimentation, we stumbled on something interesting: exchange tokens.

In order to understand how we got here, we should first take a cursory glance at how many exchange tokens work:

Keep reading with a 7-day free trial

Subscribe to The Quant's Playbook to keep reading this post and get 7 days of free access to the full post archives.