I Traded The Volatility Surface For an Entire Week — Strongly Recommend.

I like my vol surface how I like my women — curvy, kinky, and hard-to-interpret.

Some time ago, we set out to become volatility kings.

By building out our own internal volatility surface, we were able to pretty accurately predict the realized volatility of nearly every stock with listed options. While this is a fantastic ability largely attributable to the great minds before us, it raises a difficult dilemma:

You get a call telling you there’s a high chance that Boeing’s stock will move by 10% tomorrow. However, the call ends before you have a chance to hear the direction. How do you profit from this information?

This led us to search tirelessly for back-testable strategies based on surface changes; things like buying a straddle whenever the surface starts to expect significantly more short-term volatility. However, because our investable universe is so wide (every optionable stock), a purely quantitative approach completely ignores the idiosyncratic (stock-specific) factors that determine what happens next. This idiosyncratic factor is also important for deciding whether the volatility is priced too richly or cheaply — a key driver in the profitability of any options position.

So, instead of searching for a fixed, rule-based approach, what if we just went out there and traded? We’d use the volatility surface to find the dislocations and kinks, then we’d try our best to find out why the market is anticipating more/less vol for the specific stock, then finally, we’d put on a trade that supports our view.

And that’s exactly what we did.

Vol Is Kinda Thicc Sometimes

Before diving deeper, let’s first get a general idea of what we’re looking for in the surface and how we’ll trade those observations.

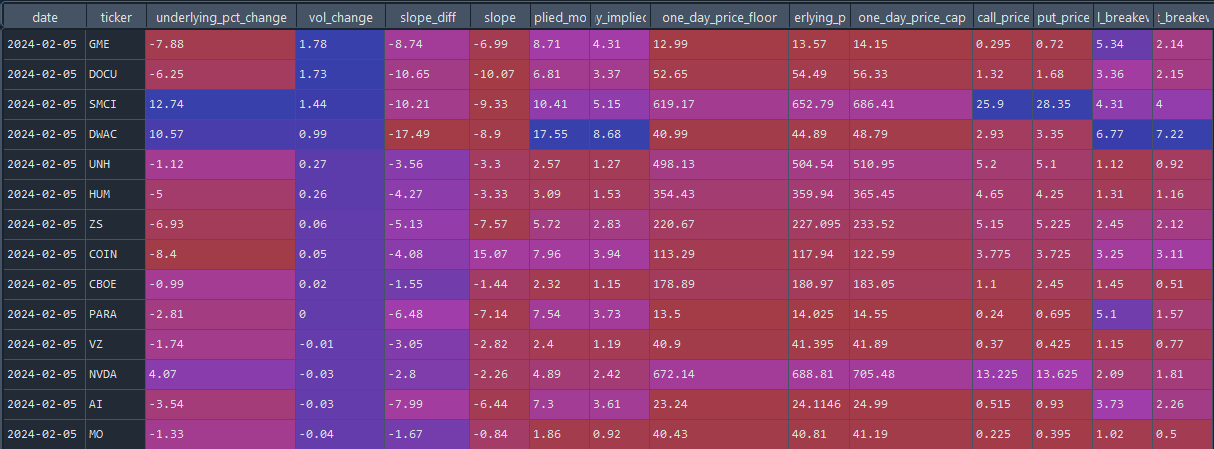

First off, here’s what our surface will look like on a typical trading day:

Our main focus is on the first 4 columns:

The underlying percent change: How the stock has performed since the prior day’s close.

Vol Change: The change in implied volatility from the prior day. If yesterday the market implied that the stock would move 5% by expiration, but today it implies that the stock will move by 7%, this is a vol change of 2%.

Slope: The IV of next week minus the IV of this week. A slope of -10% means that this week’s IV is 10% higher than the IV for the expiration of next week.

Slope diff: How much the slope has changed. If yesterday, the slope was -10% but today it’s -50%, this is a slope diff of -40.

As we’ll see later, idiosyncratic situations will lead to different kinds of trades — but in general, we will try to collect income when volatility expectations become lower, then we’ll try to long volatility when expectations become affordably higher.

Short vol scenario: Yesterday, stock ABC reported earnings and fell 10% after-hours. Upon open, implied volatility decreases and the slope normalizes to a positive value. After our review of the earnings and investor perspectives, we determine that the earnings are adequately priced-in and there isn’t likely to be any abnormal future volatility. So, we sell an iron condor right outside of the implied move (if market expects 5% vol, we sell 6% OTM iron condor).

Long vol scenario: Yesterday, Stock A, a stock in the same industry and strongly correlated to Stock B, jumped 15% after reporting earnings. Stock B plans to report earnings next week. At open, the market raises its volatility expectation for Stock B from 5% to 7% and the slope becomes negative by 10%. We take the view that Stock B’s earnings will be just as volatile and as the earnings date approaches, volatility expectations will continue to increase. So, we buy a straddle and plan to sell it before the actual earnings event.

Our volatility surface will bring these potential trades straight to us, then it’s up to us to evaluate anything out of the ordinary.

So, now that you have a general idea of how we’ll be using the surface, let’s go over some trades:

Day One - Friday

At around the close of Friday, 02/02, here’s what our curve looked like:

Keep reading with a 7-day free trial

Subscribe to The Quant's Playbook to keep reading this post and get 7 days of free access to the full post archives.