Hunting Down an ETF Arbitrage

Markets are doing something strange, let's get to the bottom of it.

While casually perusing market activity, I noticed an unusual trend in trading activity that didn’t make much sense at first:

Every day, like clockwork, there would be a surge in volume in the absolute final minutes of trading. This was most apparent in the SPDR S&P 500 ETF (SPY) and its highest constituents (e.g., AAPL, MSFT, AMZN).

With such a consistent and predictable flow of volume, it only makes sense that we first figure out who exactly is causing this flow, then once we know who/what, we can accurately estimate whether this flow will be net negative or positive, allowing us to position ourselves ahead of the move in advance for a potentially hefty profit.

So, with our mission objective set, let’s dive into the data.

Who Is Behind This?

Before figuring out exactly who’s behind this flow, we first needed to make sure that the effect was indeed real and not just a short-term visual illusion. So first, we ran data for the entire year-to-date:

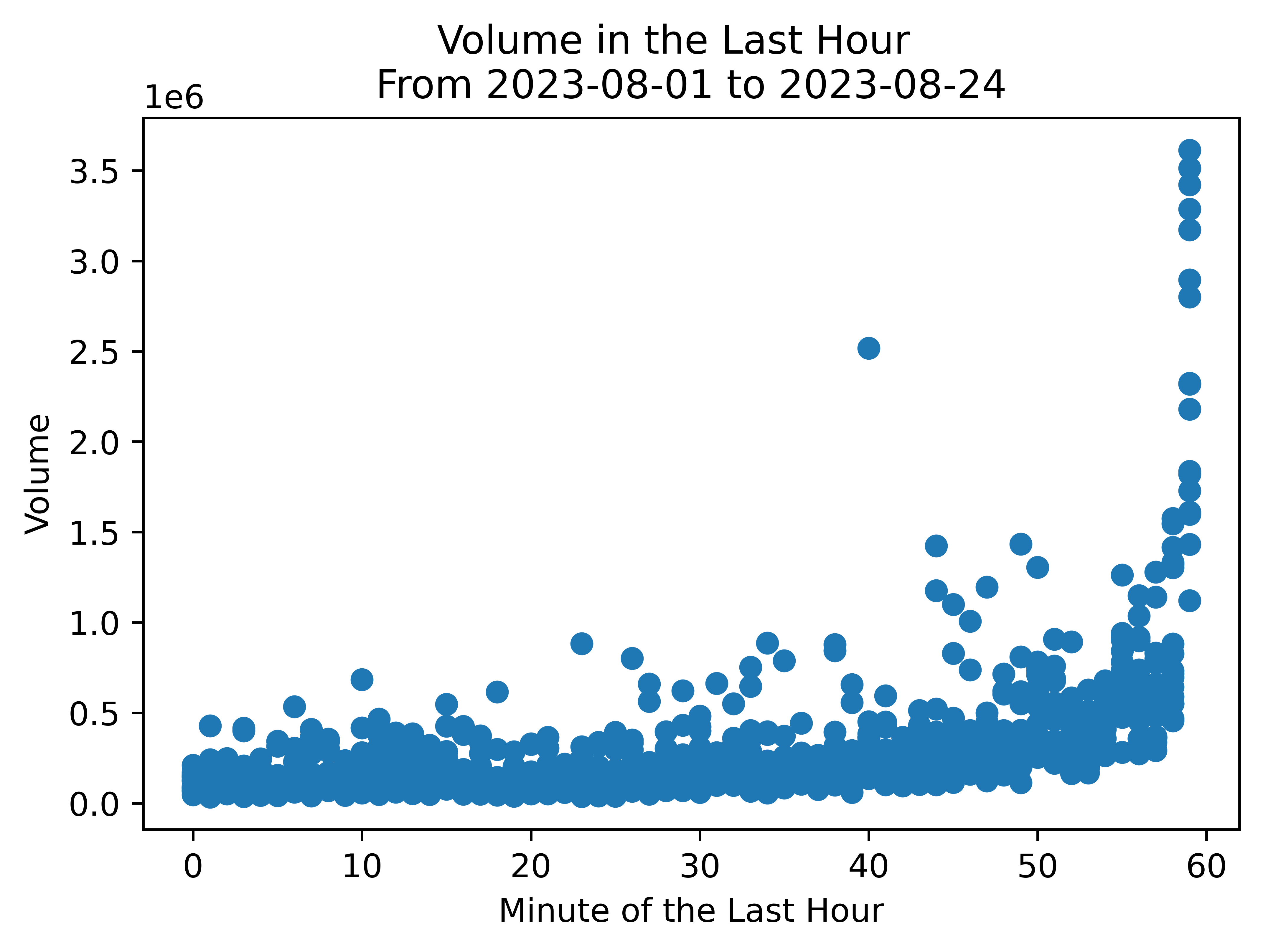

The trend is there, but let’s take a more granular view:

As demonstrated, there is a clear relationship where, as the trading session comes to a close: volume increases exponentially. So with that established, let’s review the initial candidates of who might be behind this:

Market Makers / Traders?

The theory of market makers or traders closing out their risk or delta-hedging at the end of day makes sense at first.

If a market maker sold 50,000 call options today and their net position delta is -5,000,000, they would need to buy 5,000,000 shares to offset and hedge that risk. And with new 0-DTE options, the need to deliver shares for daily exercises and hedging would possibly explain the need to trade more at the end of the day.

However, in practice, option market makers are also highly sensitive to changes in gamma, so instead of hedging through just shares, they hedge through other option contracts and futures, so the spike in volume can’t be solely attributed to a participant with those split priorities.

Furthermore, this hedging happens throughout the day continuously as it wouldn’t make sense for them to sit unhedged for the entire day, then only hedge at the last minute.

This volume occurs at the exact same time every day, so it appears that it is a rule-based criteria. So, who not only has the billions in liquidity to do this daily, but is also confined to a daily rule set?

Leveraged ETFs?

Traditional ETFs tend to rebalance on a quarterly or monthly basis, adding and removing constituents sparingly. However, leveraged ETFs have a mandate to provide a multiplier of daily intraday returns and are known to have to rebalance daily. These leveraged funds have the liquid capital commensurate with the observed volume, and rule-based rebalancing is baked into their design.

There are dozens of these ETFs, so in order for us to isolate the one responsible, we have to do a bit of leg work. Currently, the ProShares UltraPro QQQ (TQQQ) ETF represents the largest and most liquid of the bunch, with nearly $18 billion in assets under management and an average daily volume of 100,000,000 shares:

But in order for us to know if they’re behind this surge, we need to dig into their documents to search for clues into exactly how and when they rebalance. To do this, we read the through the entire prospectus.

Luckily for us, we found something.

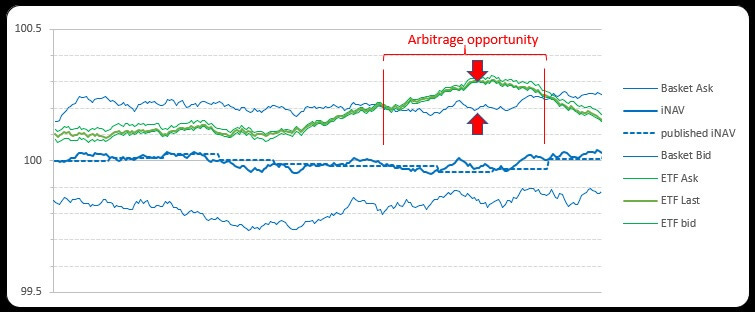

The ETF rebalances based on the NAV. For an ETF, the NAV is calculated as the total value of all constituents divided by the number of shares outstanding. When the NAV increases, the ETF has to buy more shares in the proper proportions; when the NAV decreases, they have to sell more shares:

For example, if a basket of 5 stocks is worth $100 combined individually, but the price of the ETF implies the basket is worth $99.50, the ETF is considered underexposed. This type of rebalancing happens throughout the day and is mainly arbitraged by high frequency traders:

However, if we now know that they are indeed rebalancing throughout the day to meet their outlined mandate, what other mandates do they have to meet? TQQQ is a 3x leveraged fund, so it needs to make sure that its intraday returns are as close to 3x the return of QQQ as possible. So, in theory, if they rebalance when the NAV goes out of whack, do they also rebalance when the leverage ratio goes out of whack?

The data used are 1-minute timestamps and we calculate the leverage factor as the intraday return of TQQQ / the return of QQQ. As demonstrated, they do a good job of keeping returns to the agreed upon 3x, but when that ratio goes out-of-whack (e.g., 2.90x, 3.10x), there is a significant increase in volume in the next minute.

So now that we have some insight into exactly how these ETFs trade, can we find a link that proves them responsible for the end of day volume spikes?

The Academic Connection

To find an answer, we’ll refer to the 2022 paper: The Role of Leveraged ETFs and Option Market Imbalances on End-of-Day Price Dynamics

In the paper, the authors test the theory that both market makers and leveraged ETFs are responsible for the moves, and a novel trading strategy can be deployed where we predict the direction of the volume in advanced.

Let’s break this down.

Keep reading with a 7-day free trial

Subscribe to The Quant's Playbook to keep reading this post and get 7 days of free access to the full post archives.