A Junior Quant's Guide to Scaling Up / Strategy Review

Why make one dollar, when you can make two?

You are a quant. You spend your waking hours writing code and thinking about markets. Your sole life goal is to one day use those skills to make money without talking to anyone.

After many months of accidental overfitting, unrealistic market assumptions and other statistical no-no’s, you finally find a market phenomena and start making money. Then, you make some more and then some more — and before you realize it, you’re running a pretty serious operation.

Now that you’ve reached the point of no return, you ask yourself — “How do I go BIG?”

Luckily for us, this is not a hypothetical scenario.

Today, we’ll be diving into the nuts and bolts of scaling up a real-world quantitative trading operation while also providing an update on the performance of our strategies. We’ll cover concepts ranging from market impact, to risk concentration and tailedness.

So, without further ado, let’s get into it.

If It Was Public, It Wouldn’t Work — Right?

Before we can talk about scaling up, we first need to understand our core strategies. At The Quant’s Playbook, we are currently running 3 quantitative strategies live:

Capturing the daily Variance Risk Premium

Machine-Learning Based TSLA Model

Positive EV option trades based on model prediction for the next-day direction of TSLA

Short 0-DTE SPX Iron Butterflies

Capturing the rapid end-of-day theta decay with iron butterflies

We haven’t made a dedicated post to this strategy yet, but we built, launched, and discussed it in our Discord server!

We started out with a balance of $3,000 in April 2024 and have generated a solid return on capital:

Our primary cash cow has been our short SPX volatility strategy, where we use volatility indices with a trend-following component to sell an option spread every morning at the open. So, we’ll start there.

Before figuring out how much we can scale this up by, we first have to address a rather niche concern. Many market participants adapt an ideology of “if a working strategy is made public, it will stop working.” This isn’t a totally irrational idea, but it is a bit too simplistic — to see why, let’s take a look at some data.

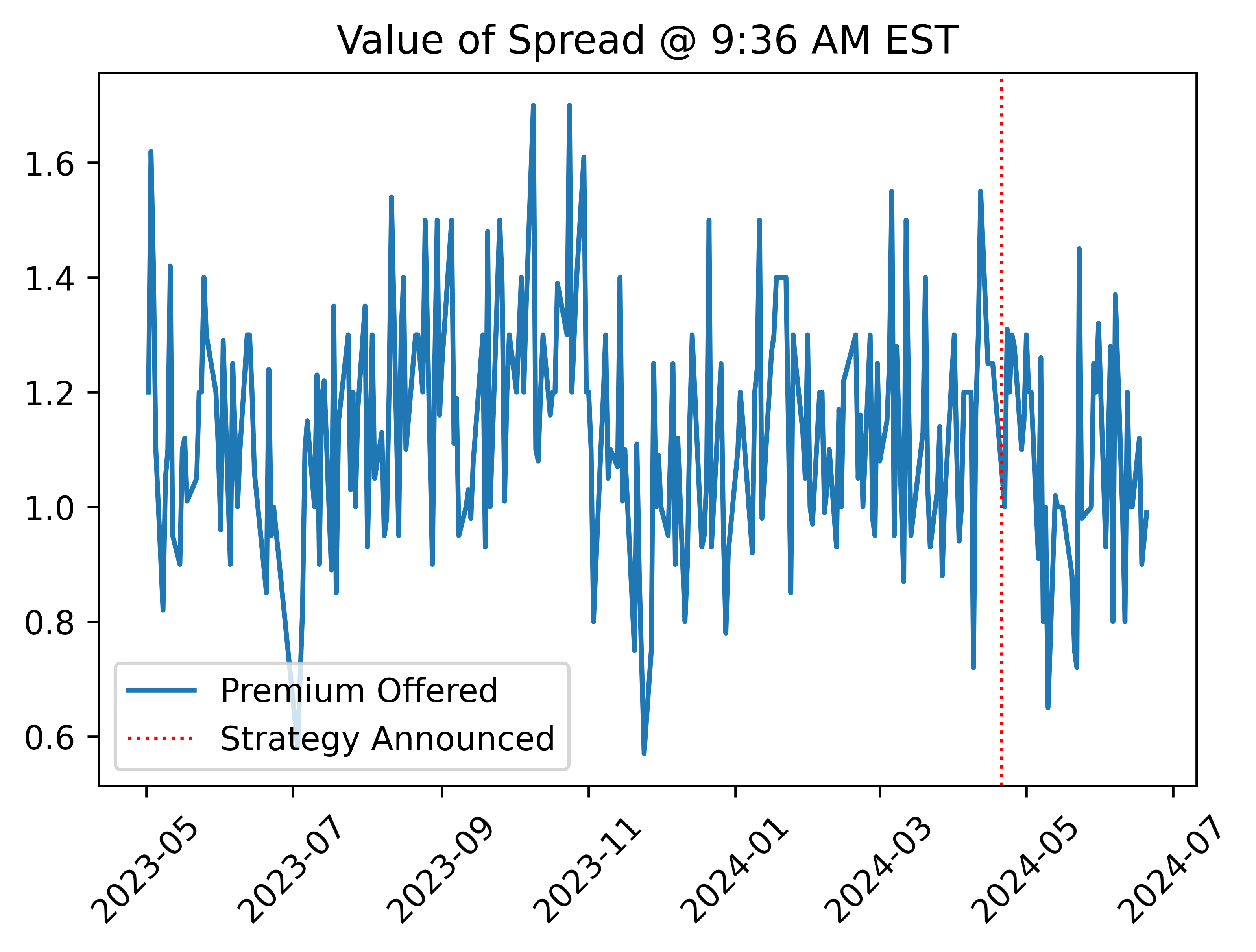

We announced our strategy on April 21st, 2024. The strategy sells option spreads, so if that prevailing theory was correct, we would expect a drop in profitability because thousands of traders would join the trade, raise the volume and ultimately make the premiums offered a lot less attractive.

Let’s see if that happened:

As demonstrated, there hasn’t been much noticeable change — there appeared to be a momentary drop in premiums offered, but that can likely be attributed to decreasing implied volatility over that same time period.

So, now that we can reasonably assume that just making our strategies public doesn’t have a noticeable market impact, we can start to test the limits.

Woah SPX, You’re Pretty Deep

Currently, we trade just 1 spread per day, but on average, there are 466 contracts of our desired strikes traded at our desired time. This means that we generally account for 0.21% of the volume at that time (1/466). Each spread has a max loss (and margin requirement) of about $400, so if we assume that 466 represents the maximum available liquidity for the spread, this implies a capacity limit of $186,400 (466*400).

Although this is just an estimate, this explains why the strategy doesn’t just get consumed by big players and evaporates. If you are a $100m fund that wants to capture the same spread by allocating $1m to the trade, you would essentially be trying to take up 10x of the available liquidity and quickly find out that there simply isn’t enough room for you.

To better visualize this, imagine the donut industry of a small town. Every day, about 10,000 donuts get sold at about $3 each for a total addressable market (TAM) of $30,000. If you’re a new mom-and-pop operator, you might enter the market with a goal of selling 500 per day, or 5% of the total market — a reasonable goal. On the other hand, if you are a multinational donut shop, you’d need to sell 50,000 per day (5x TAM) to make the operation worth it — this would be nearly impossible, so you would just skip this market entirely.

So, despite SPX being deeply liquid, the capacity constraints make this too small to be worth it for larger institutions who need huge positions to cover things like office space, lawyers, and employees. Bad for them, but perfect for us.

If we start off with a reasonable goal of 5% of the total available liquidity, this implies that we can allocate just ~$9,000 (23 contracts) to this strategy per day without a significant market impact. Scaling beyond that would likely have the market impact of lower execution prices (we’re oversupplying the buyers) and longer execution times.

Scaling to that limit would turn the strategy into a $2,300 per day operation, but even still, that’s an extremely small capacity. The goal is to make full use of all available capital, so although we hit the limit on this one strategy, we can also hit the limits of the other strategies.

Does My Left-Tail Look Big?

Although we now have a framework of estimating how much we can allocate to a given strategy, there is a major concern we must address. Short volatility strategies are infamously left-tailed (negative skew) — most days, we make say, $100, but every now and then, we lose $400:

A feature, not a bug as our win rates lead us to a positive value over time. However, the equation potentially changes when adding another short volatility strategy.

To see how, let’s walkthrough an example:

Our short butterfly strategy sells an SPX iron butterfly an hour before close and aims to buy it back at a 10% profit. On average, our max risk is $400 for a $600 credit of which we collect $60 on. The historical win rate of this approach is ~93%.

Our primary short volatility strategy sells an SPX spread at near-open for ~$100 on $400 of max risk. The historical win rate of this approach is ~82%.

We can estimate the probability of both trades winning on any given day as ~76% (.82*.93) — followed by the probability of only 1 of the trades winning as ~23% (P(AΔB)). Finally, we can estimate the probability of both trades losing on any given day as ~1% (.18*.07).

From this, we can derive the expected values of the strategies:

Vol Strategy EV = (82% * $100) + (18% * -$400) = $10

Butterfly Strategy EV = (93% * $60) + (7% * -400) = $27.8

Combined Strategy EV = (76% * 160) + (23% * -300) + (1% * -800) = $44.6

This is the final math-y concept of the day (we promise), but now that we have the probabilities and expectations of the strategies, we can pull a useful concept from our friends in the risk management department:

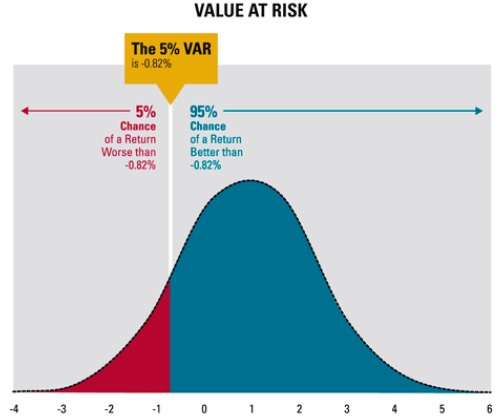

Value-at-Risk

Value-at-Risk (VaR) is simply a way of estimating our, well — value at risk:

VaR allows us to essentially have confidence intervals that reflect our risk on any given day, for instance, “with 95% confidence, we expect to not lose more than $ X on any given trading day”.

In our case, we would first calculate the standard deviation of our expected PnL outcomes:

We have a standard deviation of $211, so 68% of the time, our PnL of running both strategies will be within the bounds of $-166 to $256. We are interested in the left-tail of the distribution, so this is another way of saying “68% of the time, we won’t lose more than $166”. We can do this for 3 standard deviations which allow us to say, “99.5% of the time, we won’t lose more than $588”.

These sanity checks are important as it gives us an estimate of worst-case scenarios before we commit to scaling up. If our worse case scenario was too disastrous, we would see a lower expected value when combining strategies and choose not to scale with the secondary strategy. Further, by having a grasp on our VaR, we can fine-tune our worst-case-scenario loss by adjusting parameters (e.g. larger allocation to 1 strategy and lower to another).

Skirting Regulations

There hasn’t been much in the way of us being able to trade how we like, especially considering that the original 2 strategies trade once per day. However, since adding in the intraday butterfly strategy, we’ve had to adhere to the Pattern Day Trader (PDT) rule.

Essentially, until we have a balance >=$25,000 we are limited to 3 day-trades in a rolling 5-day period. If we sold a butterfly and bought it back in the same day, that counts as 1 day-trade.

Thankfully, getting around this is pretty easy. There is no central authority that tracks your trades, so if you use up your allotted 3 per week, you can simply go to another broker and do the same thing. The cycle is a rolling 5-day period, so you can just ping-pong back and forth between brokers every week:

Final Thoughts

While there are indeed more sophisticated measures of estimating market impact from scaling (e.g., orderbook modeling), these methods act as a solid baseline to improve on.

At The Quant’s Playbook, we strongly believe in diversification and a “never blow up” principle, so although we are looking into scaling up existing strategies, we are also continuously adding and testing new, uncorrelated strategies to better use-up our buying power. We are nearing a corner with our volatility surface approach, so it’s just a matter of time until it’s also added to the mix.

If you want to get closer to the action and discuss or ask any questions you may have regarding strategies, code, or brokers join us over at The Quant’s Playbook’s Discord! 😄

Happy trading! 😄